Best Term Life Insurance Plans Table of Contents

- 1 Why choose to get coverage via a term life insurance plan?

- 2 How do we come up with this list of the 8 best term life insurance plans in Singapore?

- 3 Best Term Life Insurance Plan for Cheapest Premium: NTUC Income TermLife Solitaire

- 4 Best Term Life Insurance Plan for Early Critical Coverage: AXA Super CritiCare

- 5 Best Term Life Insurance Plan for Lifetime Coverage: Aviva MyProtector Term Plan II

- 6 Best Term Life Insurance Plan for Optional Riders: AXA Term Protector

- 7 Best Term Life Insurance Plan for Covering Pre-existing Conditions: Prudential PRUVital Cover

- 8 Best Term Life Insurance Plan for Convertible Features: AIA Secure Flexi Term

- 9 Best Term Life Insurance Plan for Limited Premium Terms: AXA Term Protector

- 10 Best Term Life Insurance Plan for Mortgage Decreasing Term: Manulife ManuProtect Decreasing II

- 11 What other options should you consider besides term life insurance plans?

- 12 Which term life insurance plans are the most suitable for you?

InterestGuru.sg presents a comprehensive list of the best term life insurance plans and policies that provide the best value for your money.

- Best Term Life Insurance Plan for Cheapest Premium: NTUC Income TermLife Solitaire

- Best Term Life Insurance Plan for Early Critical Coverage: AXA Super CritiCare

- Best Term Life Insurance Plan for Lifetime Coverage: Aviva MyProtector Term Plan II

- Best Term Life Insurance Plan for Optional Riders: AXA Term Protector

- Best Term Life Insurance Plan for Covering Pre-existing Conditions: Prudential PRUvital cover

- Best Term Life Insurance Plan for Convertible Features: AIA Secure Flexi Term

- Best Term Life Insurance Plan for Limited Premium Terms: AXA Term Protector

- Best Term Life Insurance Plan for Mortgage – Decreasing Term: Manulife ManuProtect Decreasing II

This list of 8 Best Term Life Insurance Plan in Singapore is last updated on 06/05/2023

Why choose to get coverage via a term life insurance plan?

Term life insurance plans provide the best cost to coverage ratio, at the expense of not generating a cash surrender value for your future years. As such, it is an excellent option for those that require coverage, yet facing budget issues for financial planning.

Life situations may also have changed, resulting in the need for increased coverage due to additional financial commitments for yourself or your dependents.

While generally not meant for lifelong protection, term life plans can be a part of your financial portfolio to replace the financial losses to your income due to an unforeseen life condition.

Related article: Term Life vs Whole Life (Financial analysis and benefits comparison)

Related article: How much life insurance coverage do you need? *NEW*

How do we come up with this list of the 8 best term life insurance plans in Singapore?

Across all the insurance companies in Singapore, term life policies are each structured with their own product benefits and unique selling point.

The following criteria were considered in our review for the 8 best term life insurance plans in Singapore (2023 edition):

- Competitiveness of insurance premium

- Available options to customise and enhance coverage

- Scope of coverage for Critical Illness

- Scope of coverage for Early Critical Illness

- Terms and conditions to qualify for an insurance claim

- Product features with outstanding benefits to the policyholder

Note: This review of the 8 best term life insurance plans in Singapore is not ranked in any order of priorities or preferences.

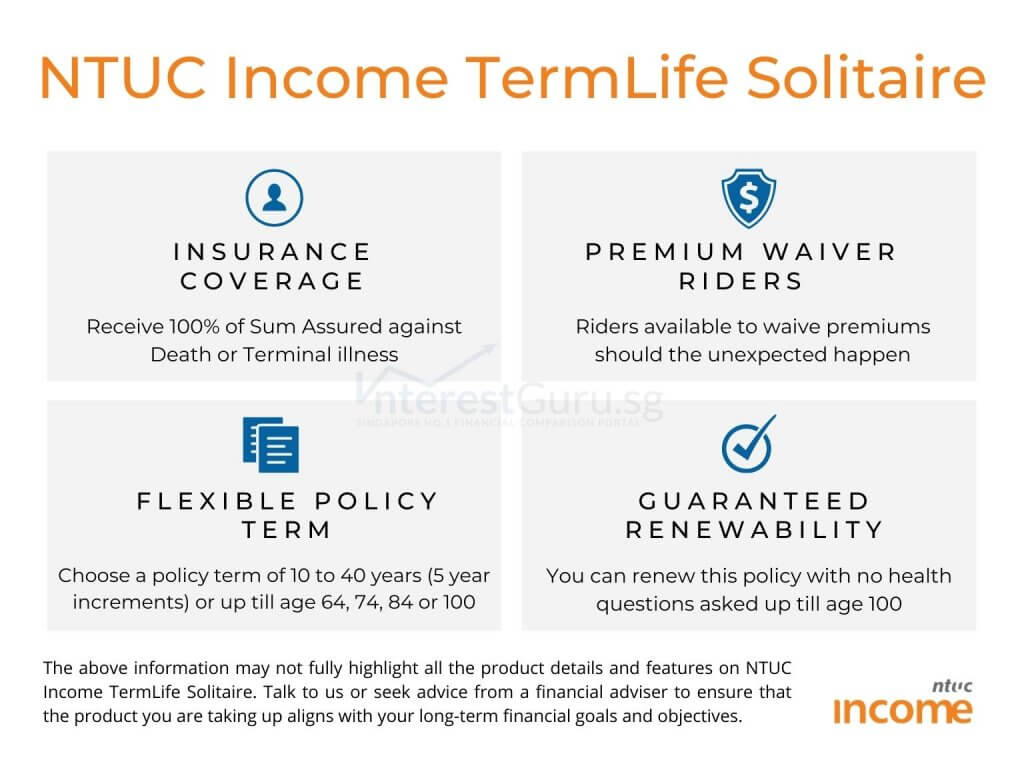

Best Term Life Insurance Plan for Cheapest Premium: NTUC Income TermLife Solitaire

NTUC Income TermLife Solitaire gives you the highest insurance coverage with the lowest premiums amongst all term life plans in Singapore.

Based on the premium payable and its definition of coverage, NTUC Income TermLife Solitaire should comfortably beat all other peers when it comes to a no-frills term life coverage.

Policy Illustration for NTUC Income TermLife Solitaire

Mary, age 33, purchase NTUC Income TermLife Solitaire to protect herself against Death and Total and Permanent Disability.

She chooses a term coverage of up to age 65 with a term coverage of S$500,000 against Death and TPD.

Mary pays a yearly premium of S$438.45 for the next 31 years up till the age of 64 to enjoy her coverage.

At age 65, Mary’s coverage will come to an end with a total of $13,591.95 paid in premiums.

Case study for NTUC Income TermLife Solitaire

Mary (female), age 33, would like to take on the following insurance coverage to age 65:

- Death: $500,000

- Total and Permanent Disability: $500,000

Sample financial Illustrations for NTUC Income TermLife Solitaire

With NTUC Income TermLife Solitaire, Mary will only be paying a premium of:

- $438.45 per year (payable until age 64)

Refer to: NTUC Income TermLife Solitaire review

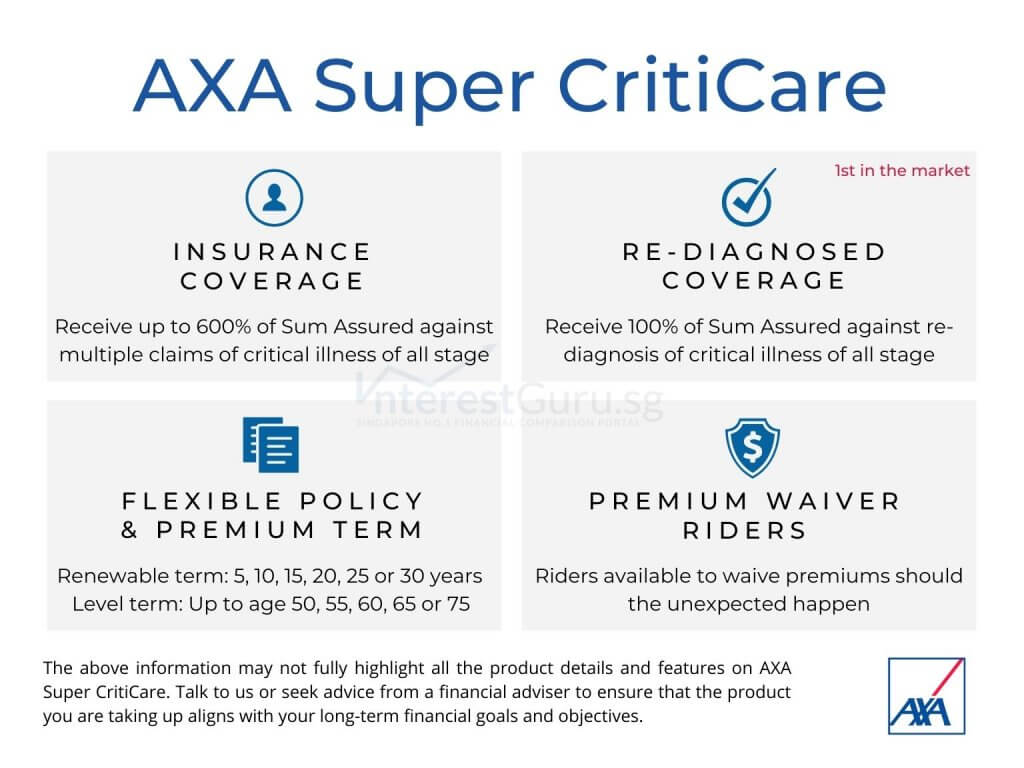

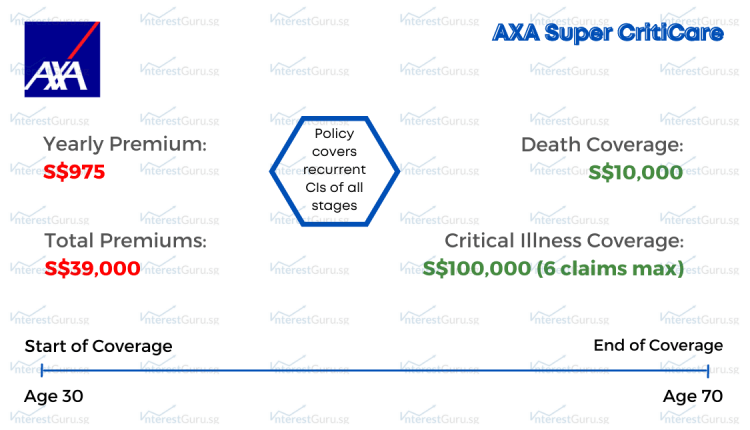

Best Term Life Insurance Plan for Early Critical Coverage: AXA Super CritiCare

Most critical illness plans in the market terminate coverage after a claim is made, but not for AXA Super CritiCare. Being one of the cheapest multipay critical illness plan in Singapore, Super CritiCare covers you up to 6 claims of critical illnesses and recurrent critical illnesses of all stages (max 600% of the Sum Assured)

Product highlights for AXA Super CritiCare

- Critical Illness Coverage – 6x claim of sum assured for any stage of critical illness (600% of the Sum Assured)

- Flexible Coverage Terms – choose to be covered a renewable term of 5 to 30 yers or up to age 50 to 75 (5-year intervals)

- Recurring Critical Illness Cover – Pays 100% of the sum assured per recurring critical illness of all stages (early, intermediate, and advanced stage)

Policy Illustration for AXA Super CritiCare

John, age 30, purchase AXA Super CritiCare to cover himself against critical illness plan and recurring critical illness plan of all stages.

He chooses to be covered with a sum assured of S$100,000 with a term coverage of up till age 70. John can make up to 6 claims of critical illnesses as well as recurring critical illness amounting to S$600,000.

John pays a yearly premium of S$975 until the age of 70, his yearly premiums do not increase even as he ages.

At age 70, John’s coverage will come to an end with a total of S$39,000 paid in premiums.

Case study for AXA Super CritiCare

John (male), age 30, would like to take up AXA Super CritiCare with a base sum assured of S$100,000 up to age 70.

John will be covered for:

- Any stage of Critical Illness (Early to advanced stage): S$100,000 per claim (up to 6 claims max)

- Recurring critical illnesses: S$100,000 (covered under the same amount of claims max for CI)

- Death benefit of S$10,000

Sample financial Illustrations for AXA Super CritiCare

With AXA Super CritiCare, he will only be paying a premium of:

- $975 per year (payable until age 70)

Refer to: AXA Super CritiCare review

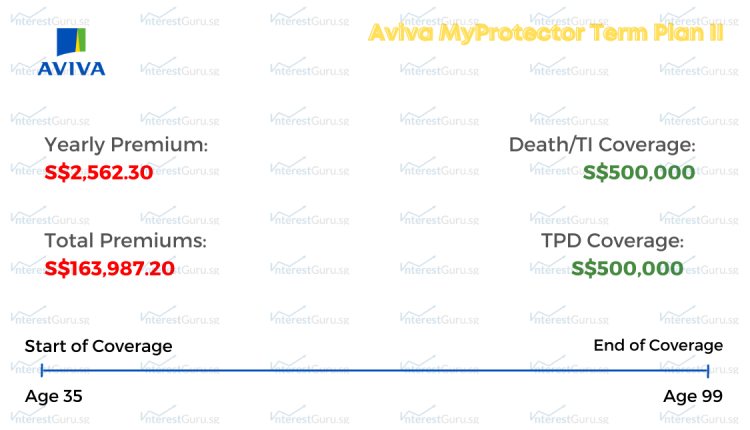

Best Term Life Insurance Plan for Lifetime Coverage: Aviva MyProtector Term Plan II

Aviva MyProtector Term Plan II has a wide range of coverage terms from 5 or 10 years, 11 years till age 85 or for a lifetime (up till age 99). Upon expiry of Aviva MyProtector Term Plan II, you can choose to extend your coverage with renewal guaranteed up to age 75.

The renewed policy will be based on the sum assured, coverage term, and age of the life assured at the time of the renewal. Policy is only guaranteed renewal if no claim has been made.

Policy Illustration for Aviva MyProtector Term Plan II

Alvin, age 35, purchases Aviva MyProtector Term Plan II to cover himself up till age 99 against Death, Terminal Illness and Total and Permanent Disability.

Alvin is eligible for the perpetual discount and pays a yearly premium of S$2,562.35 to enjoy his coverage.

If Alvin lives till age 99, his term life policy will come to an end with a total of S$163,987.20 paid in premiums.

Case study for Aviva MyProtector Term Plan II

Alvin (male), age 35, would like to provide financial assurance for his dependents in the event of his death. He chooses to get insurance coverage up till age 99 for:

- Death: $500,000

- Terminal Illness: $500,000

- Total and Permanent Disability: $500,000

Sample financial Illustrations for Aviva MyProtector Term Plan II

With Aviva MyProtector Term Plan II, he will only be paying a premium of:

- S$2,562.30 per year (after discount)

Refer to: Aviva MyProtector Term Plan II review

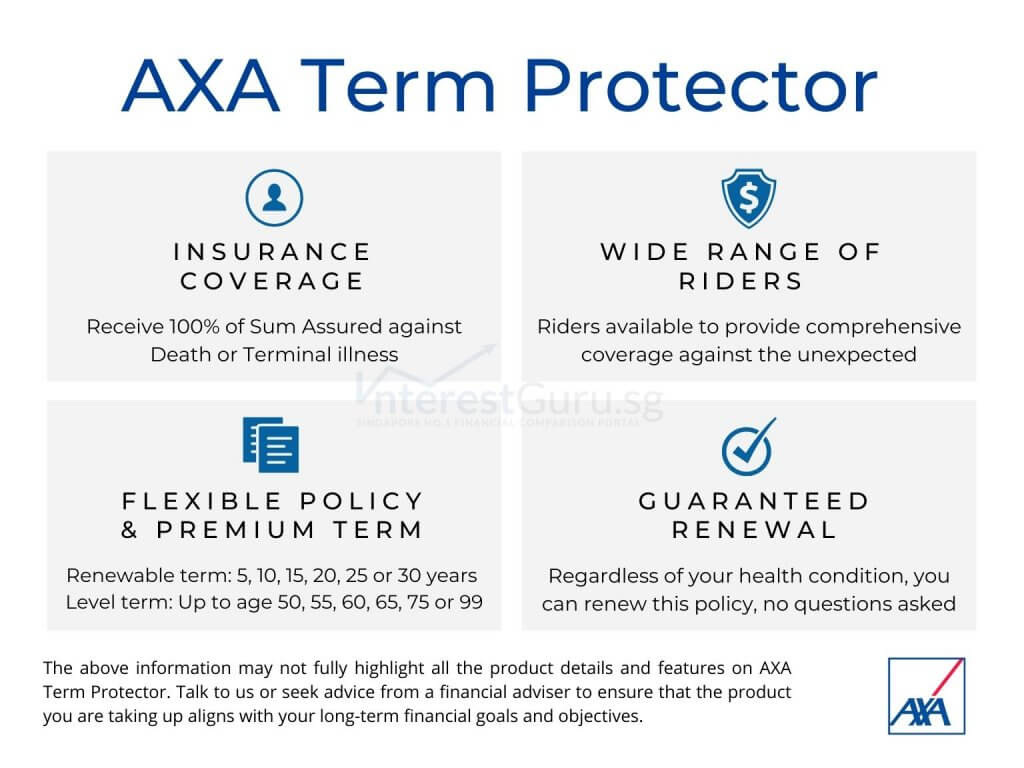

Best Term Life Insurance Plan for Optional Riders: AXA Term Protector

AXA Term Protector stands out as a flexible term life insurance plan that offers a wide range of attachable riders at a competitive premium rate.

Not only can you separately add-on riders for the conditions that you wish to be covered for, but you can also individually choose the length of coverage for each of the riders.

The following riders can be attached to your AXA Term Protector:

- Early CI Payout – Advances out your chosen sum assured if critical illness of any stage occurs

- Advance TPD Payout – Advances out your chosen death sum assured if TPD occurs

- Advance CI Payout – Advances out your chosen sum assured if critical illness occurs

- Super CritiCare – Pays you up to 600% of the sum assured against multiple claims of critical illness fo all stages

- DisabilityCash Benefit – Pays your chosen annual benefit if TPD occurs before age 60, and payable up to age 65

- Critical Illness Plus – Pays your chosen additional sum assured if advance stage critical illness occurs

- Personal Accident Benefit – Pays your chosen sum assured if accidental death or injuries occur

- Guaranteed Survival Payout – Pays your chosen sum assured if you live till the end of the coverage term

- Critical Illness Premium Eraser – Waives off your premium if critical illness occurs

- Premium Waiver(s) – Riders that waive off your premiums when critical illness, loss of income, disability, or retrenchment occurs.

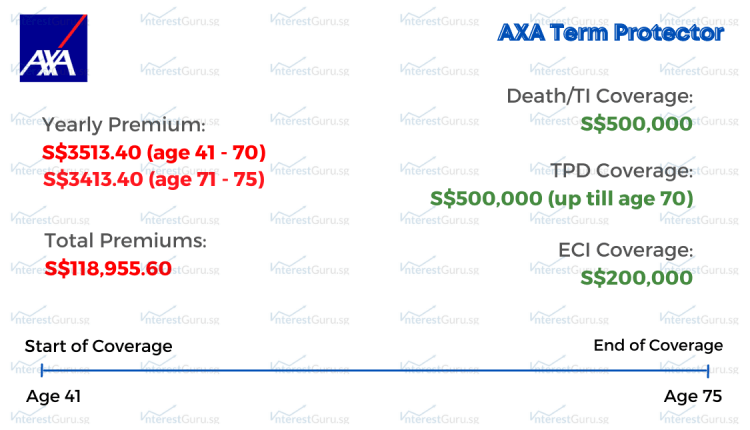

Policy Illustration for AXA Term Protector

Alvin, age 41, purchases AXA Term Protector with these add-ons: TPD (till age 70), Early CI, and Super CritiCare.

Alvin is covered S$500,000 against TPD (till age 70), Death and Terminal Illness as well as S$200,000 against Early Critical Illness and S$100,000 against Critical Illnesses (Super CritiCare, max 600% of Sum Assured)

For his coverage, Alvin pays a yearly premium of S$3513.40 up till age 70 when his TPD coverage ends. Thereafter, Alvin’s yearly premiums go down to S$3,413.40 until age 75.

Case study for AXA Term Protector

Alvin (male), age 41, would like to be covered for a $500,000 death and total permanent disability coverage. He would also like to be covered for early critical illness and critical illness.

Alvin opts for the following term coverage to age 75:

- Death: S$500,000

- Total and Permanent Disability: S$500,000 (till age 70)

- Early Critical Illness: S$100,000

- Super CritiCare: S$100,000

Sample financial Illustrations for AXA Term Protector

With AXA Term Protector and attachable riders to cover the above, Alvin will be paying a premium of:

- $3,413.40 per year (payable until age 75)

Optional Riders for Alvin

Should Alvin choose to add additional riders, the following will be the coverage and costs:

- Advance CI Payout, Sum Assured (SA) of S$200,000 – S$467.56 per year till age 70

- DisabilityCash Benefit, SA of S$5,000 – S$3.50 per year till age 60

- Critical Illness Plus, SA of S$100,000 – S$996 per year till age 75

- Personal Accident Benefit, SA of S$200,000 – S$800 per year till age 65

- Premium Waiver (UN) – S$81.60 per year till age 50

Refer to: AXA Term Protector review

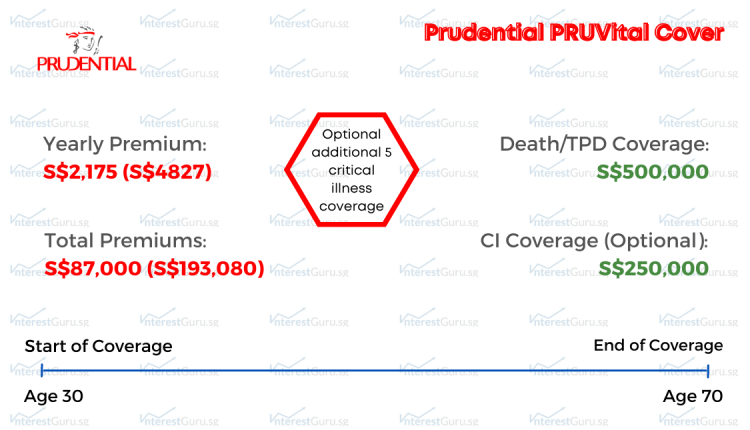

Best Term Life Insurance Plan for Covering Pre-existing Conditions: Prudential PRUVital Cover

With simplified underwriting, Prudential PRUvital Cover is a regular premium term plan that provides coverage even if you are diagnosed with the following existing medical conditions:

- High blood pressure

- High Body Mass Index

- High cholesterol

- Type 2 diabetes

It is a well-known fact that existing conditions will make getting protection coverage challenging. Furthermore, rising medical costs can and will put a financial strain on you and your family, if unforeseen events occur.

Enhance the base coverage of PRUVital Cover with riders to get protection against total permanent disability and the following 5 selected critical illness:

- Blindness

- Heart attack

- Stroke

- Cancer

- Kidney failure

Policy Illustration for Prudential PRUVital Cover

Mary, age 30, has a pre-existing medical condition. She purchases Prudential PRUVital Cover to cover herself against Death, Total and Permanent Disability (TPD), and Critical Illness.

Mary, age 30, has a pre-existing medical condition. She purchases Prudential PRUVital Cover to cover herself against Death, Total and Permanent Disability (TPD), and Critical Illness.

For just the death and TPD coverage, her yearly premium is S$2,175. But because Mary wishes to be protected against the 5 Critical Illness, she will pay a yearly premium of S$4,827 for the next 40 years.

At age 70, Mary’s term life policy will come to an end with a total of S$193,080 paid in premiums.

Case study for Prudential PRUVital Cover

Mary (female) with existing conditions, age 30, would like to ensure that there is no financial disruption to her family and dependents in the event of her demise. She is also considering getting coverage for a lump sum payout for specific critical illness.

Mary would like to take on the following insurance coverage to age 70:

- Death: $500,000

- Total and Permanent Disability: $500,000

- Critical Illness: $250,000 (Optional)

Sample financial Illustrations for Prudential PRUVital Cover

With Prudential PRUVital Cover, she will be paying a premium of:

- $2,175 per year (payable until age 70), only for Death and TPD coverage

- $4,827 per year (payable until age 70), with optional coverage for 5 selected Critical Illness

Refer to: Prudential PRUvital cover review

More about: PRUvital cover: Insurance coverage for pre-existing medical conditions

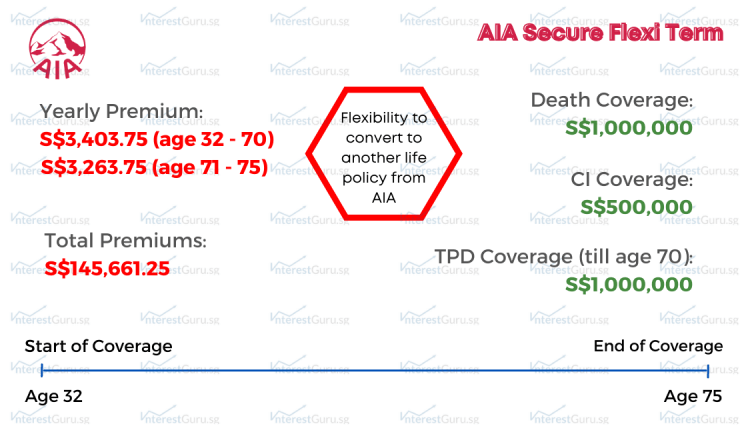

Best Term Life Insurance Plan for Convertible Features: AIA Secure Flexi Term

AIA Secure Flexi Term allows you to convert your policy with no evidence of health to any available AIA life insurance plan.

The plan can be converted to an endowment, investment-linked policy, or whole life plan offered by AIA before age 70, with no regard to your health condition.

Why is AIA Secure Flexi Term highlighted for its convertible features?

The policies that you can covert your AIA Secure Flexi Term into are featured in our other reviews due to outstanding benefits. Options include and are not limited to the following:

- AIA Smart Flexi Rewards (Featured in “hyperlink new best endowment article”)

Policy Illustration for AIA Secure Flexi Term

Jack, age 32, purchase AIA Secure Flexi Term till age 75 to cover himself against Death, Total and Permanent Disability, and Critical Illness.

He chooses a term coverage of S$1,000,000 against Death and Total and Permanent Disability (till age 70) and S$500,000 against Critical Illness.

From age 32 to 70, Jack pays a yearly premium of S$3,403.75. Jack’s TPD coverage then ends, bringing his yearly premium down to S$3,263.75 till age 75.

At age 75, Jack’s AIA Secure Flexi Term policy comes to an end with a total of S$145,661.25 paid in premiums.

Case study for AIA Secure Flexi Term

Jack (male), age 32, would like to take on the following insurance coverage to age 75:

- Death: S$1,000,000

- Total and Permanent Disability (till age 70): $1,000,000

- Critical Illness: $500,000

Before age 70, Jack can convert his term life policy to a protection plan that can accumulate cash values, while retaining his coverage regardless of his health condition.

Sample financial Illustrations for AIA Secure Flexi Term

With AIA Secure Flexi Term, he will be paying a premium of:

- $3,403.75 per year (payable until age 70)

- $3,263.75 per year (payable from age 71 to 75)

Refer to: AIA Secure Flexi Term review

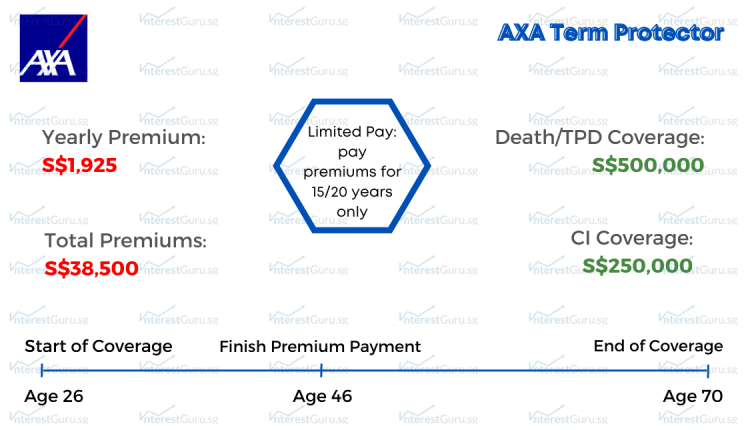

Best Term Life Insurance Plan for Limited Premium Terms: AXA Term Protector

The only term plan in the list that is mentioned twice, AXA Term Protector allows you to pay your premiums for either 15 or 20 years and get term coverage to your desired age.

This allows you to pay premiums when you are still earning an income, instead of until the end of the policy.

Policy Illustration for AXA Term Protector – Limited Pay

Derrick, age 26, purchase AXA Term Protector with a limited premium payment term of 20 years. This means that Derrick only pays premiums for 20 years but enjoys coverage up till age 70.

Derrick chooses to be covered S$500,000 against Death and Total and Permanent Disability, and S$250,000 against Critical Illness.

Derricks pays a yearly premium of S$1,925 for the next 20 years. He finishes premium payment at age 46 with a total of S$38,500 paid in premiums.

At age 70, Derrick’s AXA Term Protector policy will come to an end. There is no maturity or cash value as this is a term life plan and not a whole life plan.

Case study for AXA Term Protector – Limited Pay

Derrick (male), age 26, would only wish to pay an insurance premium for 20 years and get coverage to age 70 for:

- Death: $500,000

- Total and Permanent Disability: $500,000

- Critical Illness: $250,000

Derrick would finish paying the premiums by the age of 46 and be covered all the way to age 70.

Sample financial Illustrations for AXA Term Protector – Limited Pay

With AXA Term Protector, he will only be paying a premium of:

- $1,925 per year (payable until age 46)

His coverage will last all the way until age 70, despite only paying an insurance premium for 20 years.

Refer to: AXA Term Protector review

Best Term Life Insurance Plan for Mortgage Decreasing Term: Manulife ManuProtect Decreasing II

ManuProtect Decreasing II is a term life plan that’s purposed to cover the loan taken against your home. Premiums remain the same throughout the term while the coverage decreases year by year.

The joint lives assured option lets both you and your spouse be covered by the same plan. You can also choose a loan interest of 1%, 2%, 3% 4%, or 5% to ensure that your mortgage is adequately covered.

Refer to: Manulife ManuProtect Decreasing II review

What other options should you consider besides term life insurance plans?

If coverage is only required for a short time period, the insurance premium paid for a term life plan will be the lowest compared to other insurance policies.

Your age, budget, coverage period and investment risk appetite may result in alternative options that provide better value for your money.

You may wish to consider the following life insurance policies that provide high insurance coverage and wealth accumulation features:

- Whole Life Plans – Lifelong coverage with stable wealth accumulation

- Investment Linked Policies – Coverage with potential high investment returns

Read about: 3 things to consider before taking up a new financial product

Read about: 8 commonly made financial mistakes by Singaporeans

An alternative to term life insurance plans: Whole life plans

In your 20s or early 30s, the total premium paid over a limited period for lifetime coverage may end up being lower compared to a term life plan. Not only is the overall premium lower, but a whole life plan will also accumulate a guaranteed cash value that increases over time.be

The accumulated cash value can be withdrawn at your later life stages for other financial goals, such as a lump sum retirement payout or a monthly income stream.

Read about: 4 Best Whole Life Plans for Coverage and Wealth Accumulation (2023 Edition)

Read about: 8 Best Whole Life Plans in Singapore based on Product Features (2023 Edition)

An alternative to term life insurance plans: Investment linked policies

Investment linked policies (ILPs) combines elements of insurance and investment to provide coverage and projected investment returns. An attractive feature of ILPs is that cash can be withdrawn from the available cash value within the policy.

Unlike a whole life plan, the cash value in ILPs is based on projections of investment returns. This projected financial cash values may have high fluctuations and such policies may not be suitable if you are reluctant to take on any form of risks.

Read about: 3 Best Investment Linked Policies in Singapore for Coverage and Wealth Accumulation (2023 Edition)

Which term life insurance plans are the most suitable for you?

Contact us using the form below and our panel of partnered financial planners will advise accordingly, based on your financial profile and protection needs.

All proposals provided are 100% free of charge with no obligation to take up any proposed financial products or services in any way.

*For a limited time, get attractive incentives when you take up any products that is proposed by our team of financial planners.

We compare term life plans from all leading insurers in Singapore!

Too much work to fill in the form above?

Drop us a message and let InterestGuru.sg contact you instead. We may assign one of the licensed financial advisers to work on your inquiry at no cost to you.

Best Insurance Plans in Singapore

Note: All financial figures are based on close approximate and all non-guaranteed figures are based on the higher tier of 4.75% investment returns. The sample illustrations are for illustrative purposes only and is not a contract of insurance. Early surrendering or cashing out from a life insurance policy will certainly result in financial losses. In the event of doubt, always refer to the precise terms and conditions as specified in your policy contract. Seek the advice of a qualified financial professional or a licensed financial adviser before making any decision or financial commitment.

*Terms and conditions may apply, speak to our financial planners or drop us a message for more details.