You may have heard it on the news, from your friends and family, or got the letter, one way or another, it’s brought you here so let’s understand everything you need to know about CareShield Life and CareShield Life supplements.

In this article, you will learn everything about CareShield Life (Singapore’s new national disability income plan), what it can do for you, and what do you need to do about it, and how you can increase the payouts should you become disabled.

DO YOU KNOW: 1 in 2 healthy Singaporeans aged 65 could become severely disabled in their lifetime, and may need long-term care. Severe disability may arise due to a sudden disabling event (e.g. stroke and spinal cord injuries), the worsening of chronic conditions and diseases (e.g. diabetes), or the progression of illnesses as we age (e.g. dementia).

CareShield Life at a glance

The following are the key takeaways about CareShield Life which you should know. Each of the following points will be explained in-depth in the post:

- Provides monthly income in the event of severe disability (S$600 – S$1200)

- Auto-enrollment for Singaporeans born on and after 1980

- Optional upgrade for Singapore born before 1979

- Payout increases based on years of the insurance premium paid

- All future insurance premium waived upon a successful claim

- Provides higher monthly payout compared to existing ElderShield 300/ 400

You will also get a clear understanding of CareShield Life via the following commonly asked questions:

- Why is there a need for CareShield Life (and why do you need it)?

- Are you currently covered by CareShield Life (and how to apply for it)?

- What is the insurance premium for CareShield Life (and which scheme are you on)?

- What are the benefits of CareShield Life (Is it better than ElderShield 300/ ElderShield 400)?

- How can you qualify for a successful claim?

- How can you upgrade your CareShield Life for a higher claim payout (Higher protection in the event of disability)?

Why is there a need for CareShield Life?

CareShield Life is a government-initiated disability insurance plan that takes effect on the 1st of October 2023. This disability insurance plan replaces the previous ElderShield 300 and ElderShield 400.

Key features of CareShield Life

As an upgrade over ElderShield 300 and ElderShield 400, your CareShield Life offers:

- Lifetime income payout as long as u are severely disabled

- Higher minimum payout starting at $600 monthly

- Higher maximum payout of up to $1,200 monthly

- Lower monthly insurance premium as premiums are spread out over a longer period of time

“As our population ages, we want to ensure that Singaporeans continue to have accessible and affordable long-term care. With CareShield Life, severely disabled Singaporeans can be assured that they will receive financial support for life.

CareShield Life offers you worldwide coverage against severe disability in the form of lifetime monthly payouts for as long as you remain severely disabled. Claims can be made in the form of a lifetime monthly payout, and the disability income payout will be provided regardless of your current place of residence.

Are you covered under CareShield Life?

CareShield Life is mandatory for those aged 40 and under in 2023 and will automatically cover all Singaporeans turning 30 from here on out, regardless of any existing medical conditions or disability.

Depending on your age, your enrollment into CareShield Life will be as follows:

Born after 1990 – If you are a Singaporean below age 30 in 2023, you’ll be automatically enrolled in CareShield Life when you reach the age of 30 even if you have any existing medical conditions or disabilities.

Born between 1980 and 1990 – If you are a Singaporean between the age of 30 and 40 in 2023, you’ve been automatically enrolled in CareShield Life even if you have any existing medical conditions or disabilities.

Born between 1970 and 1979 – If you are a Singaporean age 41 to 50 years old in 2023 and already on ElderShield 400 and not severely disabled, you will be automatically enrolled in CareShield Life from end-2023. You can choose to opt-out by 31st December 2023 if you do not wish to remain on CareShield Life.

If you were born before 1979 – If you are 41 years old and above in 2023, you have an option to join CareShield Life from end-2023 onwards, if you are not severely disabled.

For existing ElderShield 300 and ElderShield 400 members with or without ElderShield Supplements(rider) and do not wish to join CareShield Life, your existing coverage will continue and will not be affected.

Insurance premiums for CareShield Life

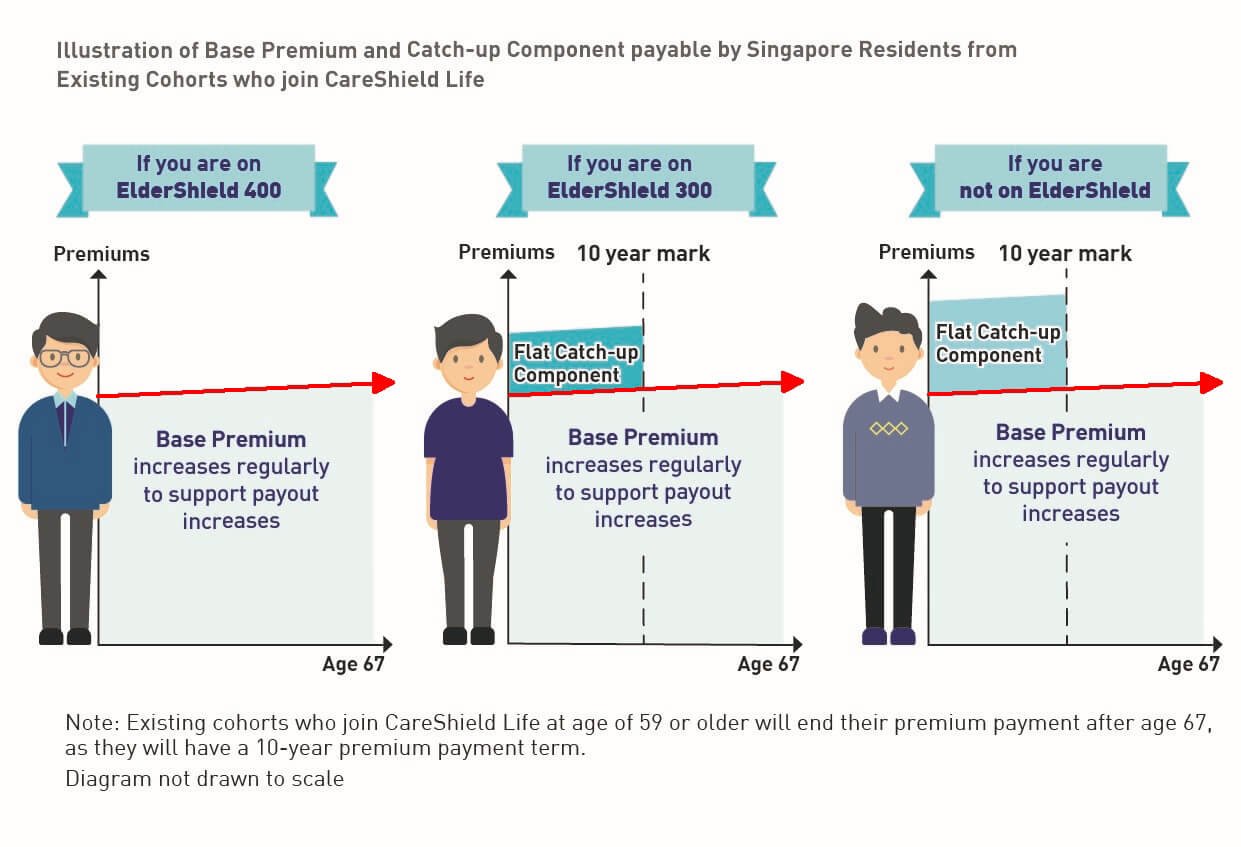

Depending on your current age, you may have to pay either a base premium or a base premium and a catch-up component. Refer to the following to find out which group you below to:

If you are born in 1980 or later

You pay only a base premium from the age that you join until the age of 67 (inclusive of the year you turn age 67), and you remain covered for life. From 2023 to 2028, it is confirmed that the base premiums and payouts will both increase by 2% per year. From 2029 onwards, premium and payout adjustments will be recommended by an independent CareShield Life Council.

Currently, annual premiums for CareShield Life starts at $206 for males and $253 for females and is fully payable with MediSave until the age of 67. No further premium or deduction will be required by your last premium

CareShield Life premium calculator (Born in 1980 or later) – Login with your SingPass to find out the exact premium payable based on your profile.

If you are born in 1979 or earlier

Your insurance premium for ShieldCare Life may consist of 2 components, namely the Base Premium and the Catch-up Component.

Born in 1979 or earlier – Do you have to pay the base premium?

All Singaporeans born in 1979 or earlier and who join CareShield Life will have to pay a base premium. Base premiums are paid from the age you join until age 67 (inclusive of the year you turn age 67), or for a period of 10 years for those who join CareShield Life at age 59 or older, in end-2021.*

If you have consistently been on ElderShield 400, have never opted out of ElderShield, or upgraded from ElderShield 300 to ElderShield 400 in 2007, the base premium will be all you need to pay for CareShield Life, provided you enroll by the end of 2023.

Born in 1979 or earlier – Do you have to pay the Catch-up Component?

For existing ElderShield 300 policyholders, those not insured under ElderShield, and those who opted into ElderShield late, you will need to pay an additional catch-up component, as you would not have paid as much insurance premiums as your peers who had been consistently insured under the ElderShield 400 scheme.

This catch-up component is a flat fee paid yearly over the span of 10 years, on top of the base premium to ensure you receive sufficient coverage and balance in premiums paid for CareShield Life.

CareShield Life premium calculator (Born in 1979 or earlier) – Check the exact insurance premium payable by providing the following details (Birth Year, Gender, Citizenship, Monthly Per Capita Household Income, Current ElderShield Coverage, and Housing Type).

How does CareShield Life fair against ElderShield?

CareShield Life was designed to provide you with a higher level of protection compared to the previous national disability insurance plan known as ElderShield 300 or ElderShield 400. This is especially important with medical advancements resulting in a high life expectancy globally.

DO YOU KNOW: Singapore topped the world in life expectancy in 2017 with an expected lifespan at birth of 84.8 years, surging ahead of traditional chart-topper Japan by more than half a year.

What makes CareShield Life outstanding is that this plan provides income for a lifetime, with all future premiums waived upon disability. Comparing affordability (premiums you pay) against coverage (disability income payout), CareShield Life will outperform the previous ElderShield 300 and ElderShield 400 by a landslide.

One of the key reasons why it is so competitive is that you start paying premiums from the age of 30 for CareShield Life, instead of from age 40. The longer period of payment makes the monthly premiums lower for a comparable higher payout for a lifetime.

How much premium do you pay for CareShield Life compare to ElderShield?

Under the old ElderShield 300 and ElderShield 400 scheme, you would have paid the following assuming entry at the age of 40:

For ElderShield 400: $174.96 (Males) and $217.76 (Females) yearly over 26 years. The total premium you would have paid would be a total of $4,548.96 and $5,661.76 respectively.

For ElderShield 300: $151.67 (Males) and $194.26 (Females) yearly over 26 years. The total premium you would have paid would be a total of $3,943.42 and $5,050.76 respectively.

With the new and enhanced CareShield Life, you pay $206 (Males) and $253 (Females) yearly from the age of 30 to 67. The total premium you would have paid would be a total of $7,622 and $9, 361 respectively.

While the total premium paid for CareShield Life would be higher compared to ElderShield over the policy lifetime, the payout benefits of CareShield Life cannot be understated.

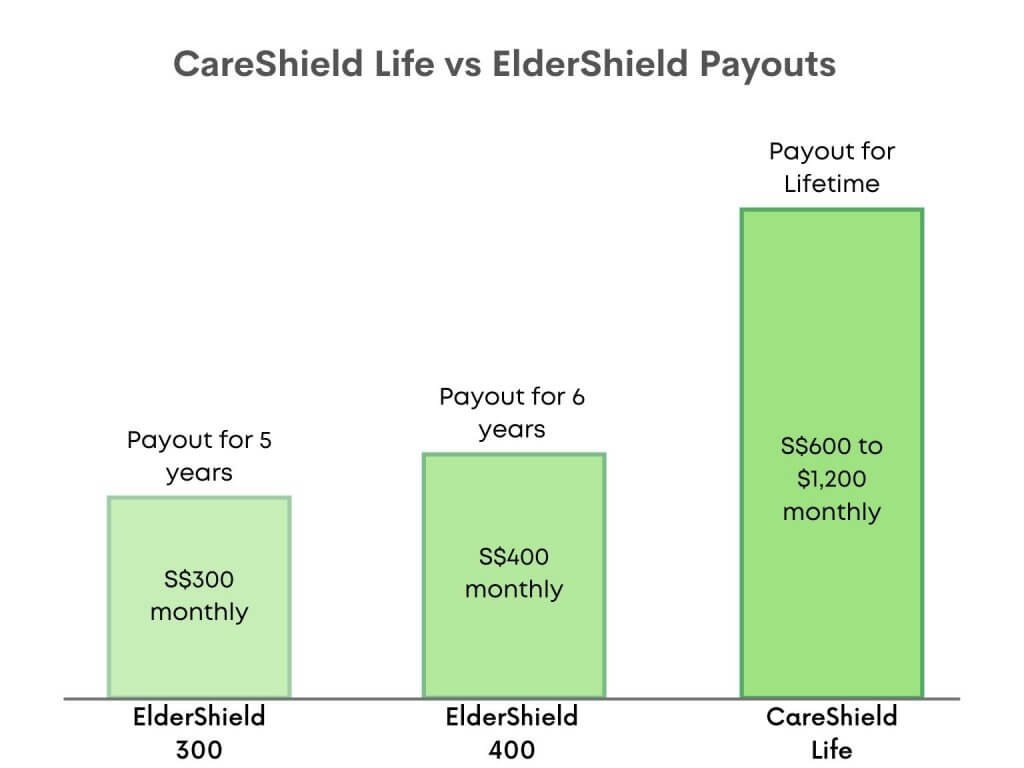

What are ElderShield and CareShield payouts like?

- With Eldershield 300 – You will get $300 per month for 60 months, in the event of severe disability.

- With ElderShield 400 – You will get $400 per month for 72 months, in the event of severe disability.

- With CareShield Life – You will get a minimum payout of $600 per month for a lifetime, in the event of severe disability.

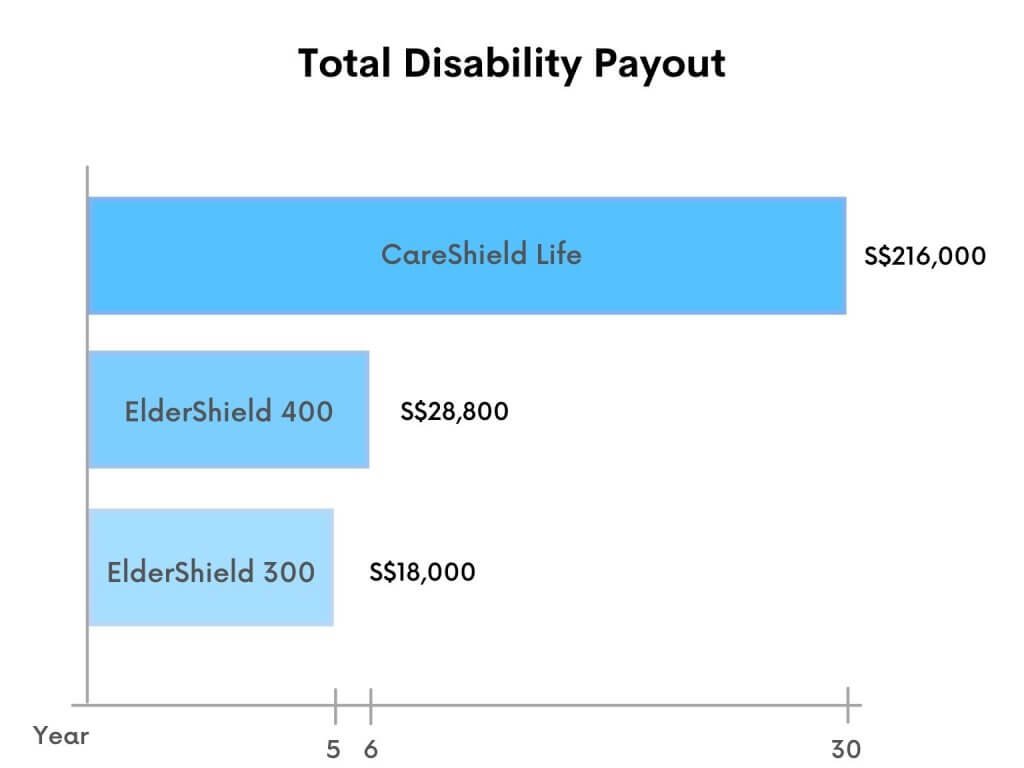

This means that in the worst or best case scenario, in the event you become severely disabled after paying only one year of premium and continue living for another 30 years, you get:

- With Eldeshield 300 – A total of S$18,000 or S$3,600 per year for the first 5 years only

- With Eldershield 400 – A total of S$28,800 or S$4,800 per year for the first 6 years only

- WIth CareShield Life – A total of S$216,000 or S$7,200 per year over the remainder of your life (30 years)

![Comparison of Total Disability Payout from Careshield Life vs ElderShield 300 and 400]()

CareShield Life payout starts from $600 per month and goes up to $1200 per month depending on the years of premiums that you have paid before becoming severely disabled and making a claim.

The below graph depicts the increasing monthly payout if the first 6 years of premiums are paid:

| Year (Assuming you join and started paying your first premium in 2020) | Monthly Payouts (S$) |

|---|---|

| 2023, 1 payment made. | S$600 monthly, for a lifetime. |

| 2024, 2 payments made. | S$612 monthly, for a lifetime. |

| 2025, 3 payments made. | S$624 monthly, for a lifetime. |

| 2026, 4 payments made. | S$637 monthly, for a lifetime. |

| 2027, 5 payments made. | S$649 monthly, for a lifetime. |

| 2028, 6 payments made. | S$662 monthly, for a lifetime. |

With the new and enhanced CareShield Life, your disability income payout starts at a minimum of $600 up to $1200 per month for a lifetime so long as you remain severely disabled, until the day you pass on.

You will receive higher coverage with more premiums paid. If and once you make a claim, your coverage amount or monthly disability payout will be set in stone and all future premiums will be waived.

As seen from the example above, CareShield Life greatly exceeds ElderShield 300 or ElderShield 400 in terms of length of income payout as well the payout amount.

Are the premiums for CareShield Life fixed?

Premiums and payouts are both set to increase by 2% a year from 2023 to 2028. Thereafter, any adjustments in premiums and payout will be recommended under the good judgments of an independent CareShield Life Council

Are there incentives for joining CareShield Life?

If you were born after 1979 and decide to be enrolled in CareShield Life within the first 2 years of the launch (October 2023), there will be an incentive to join with subsidies ranging from $50 to $250 per year for 10 years, depending on your age.

How do I make a successful claim?

To make a successful claim, the applicant must be deemed severely disabled. In Singapore, one has to lose the ability to carry out at least 3 of 6 Activities of Daily Living (ADLs) independently.

The 6 Activities of Daily Living (ADLs) are:

- Washing (cleaning yourself)

- Dressing (putting on and taking off clothes)

- Feeding (eating)

- Toileting (doing your natural business in the toilet)

- Mobility (moving around) and

- Transferring (getting off your bed)

For applicants making the first claim from CareShield Life, any fees incurred from the first assessment will be waived.

If the above is applicable to you and you are covered with CareShield Life, you may apply here.

What if CareShield Life payouts are not enough for me?

Payouts from CareShield Life alone may not be enough for your ideal healthcare and lifestyle needs in the event you become severely disabled. You should also consider getting a CareShield Life supplement plan to further boost your payouts amongst other benefits as per the individual insurers.

Instead of only being able to claim once you are severely disabled, a supplement plan starts paying out as early as if you are just moderately disabled (disability to do 2 of 6 ADLs under CareShield Life’s definition) and increased disability payout if you become severely disabled later on.

Beyond receiving a higher monthly disability payout, getting a supplement plan for your CareShield Life also means you receive earlier protection.

Another plus point is that the supplementary plans can be funded with your MediSave up to $600 per year, with the surplus amount payable in cash.

What are the CareShield Life supplements available?

These are the CareShield Life supplements currently available:

- NTUC Income Care Secure

- Aviva MyLongTermCare

- Aviva MyLongTermCare Plus

- Great Eastern GREAT CareShield Enhanced

- Great Eastern GREAT CareShield Advantage

Add on any one of these CareShield Life supplements to give you more disability income monthly in order for a more comfortable recovery.

CareShield Life Supplement – NTUC Income Care Secure

- Payout starts upon disability to do 2 of 6 ADLs

- Receive Monthly Disability Income (MDI) for as long as you remain disabled

- Receive a lump-sum 6X the MDI upon disability to do 2 of 6 ADLs

- In the event of death, receive 3X the MDI if you had made a successful claim of disability

For greater details check out the in-depth review for NTUC Income Care Secure.

CareShield Life Supplement – Aviva MyLongTermCare (MLTC)

- Payout starts upon disability to do 3 of 6 ADLs

- Receive Monthly Disability Income (MDI) for as long as you remain disabled

- Choice of fixed payout or payout that increase over time at 2/3% per annum to meet inflation

- Receive a lump-sum 3X the first MDI upon disability to do 2 of 6 ADLs

- Additional 20% of MDI if you have a child under the age of 22 (36 months max)

- Additional 60% of MDI if your condition improves but still unable to do 2 of 6 ADLs

- If you get better but still not able to do 2 of 6 ADL, MDI goes down to 50% of MDI

- Future premiums are waived once you’re unable to do 1 of 6 ADLs

- Lump-sum payout 3X the last MDI should death occur

For greater details check out the in-depth review for Aviva MyLongTermCare.

CareShield Life Supplement – Aviva MyLongTermCare Plus (MLTC+)

- Payout starts upon disability to do 2 of 6 ADLs instead of MLTC 3 of 6 ADLs

- Everything in MyLongTermCare

For greater details check out the in-depth review for Aviva MyLongTermCare Plus.

CareShield Life Supplement – Great Eastern GREAT CareShield Enhanced

- Payout starts upon disability to do 2 of 6 ADLs (50% of MDI)

- Payout increases upon disability to do 3 of 6 ADLs (100% of MDI)

- Future premiums are waived upon disability to do 1 of 6 ADLs

- Premiums stays the same throughout the term

For greater details check out the in-depth review for Great Eastern GREAT CareShield Enhanced

CareShield Life Supplement – Great Eastern GREAT CareShield Advantage

- Includes everything in GREAT CareShield Enhanced but

- Payout starts upon disability to do 2 of 6 ADLs (100% of MDI)

- Receive a lump-sum 3X of the MDI upon disability to do 1 of 6 ADLs

For greater details check out the in-depth review for Great Eastern GREAT CareShield Advantage.

Conclusion

Considering the statistics of possibilities that come with old age and the increasing cost of health care in Singapore, it truly pays to be protected against what is likely to happen. In the unfortunate event of becoming severely disabled, having the financial burdens of health care upon other family burdens only adds insult to injury.

Having a disability insurance plan that pays out lifetime disability income that’s not funded out of your physical pocket relieves any stress from your overall financial goals.

Drop us a message and let our team of qualified advisers address your disability income needs accordingly.