🧓 A Looming Challenge for Ageing Singapore

As Singapore’s population ages rapidly, long-term care (LTC) is becoming an urgent and deeply personal issue. From stroke recovery to dementia and frailty in old age, more citizens will eventually need help with daily living. The critical question is: Are we financially prepared for it?

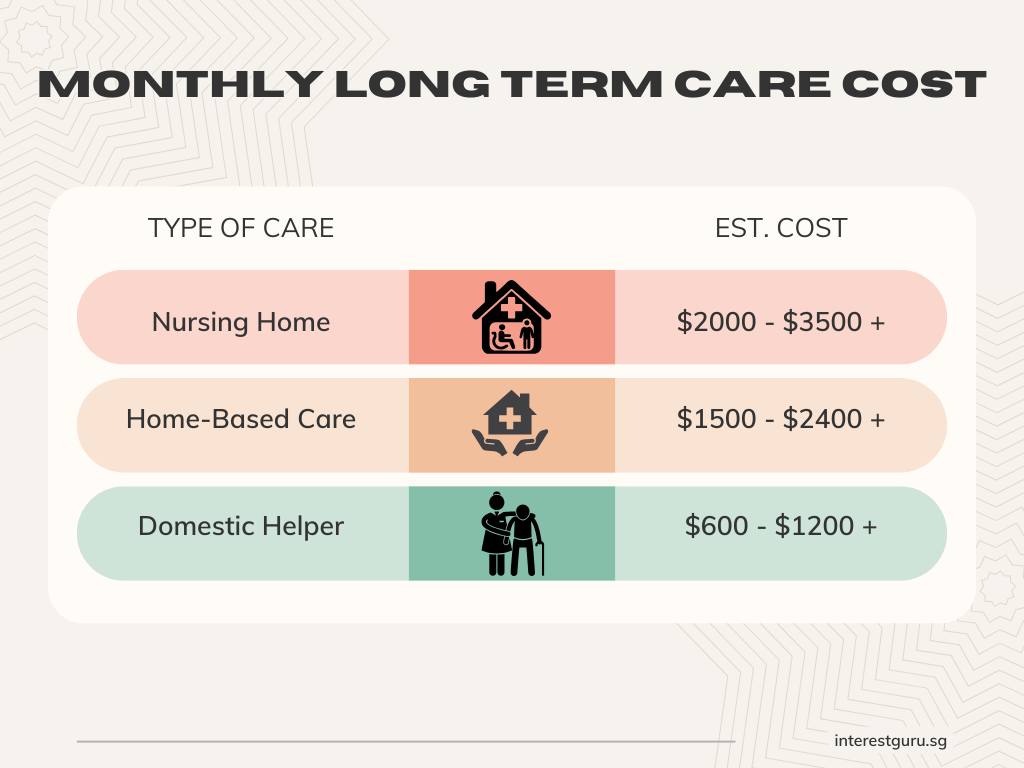

💸 The High Cost of Long-Term Care in Singapore

Long-term care isn’t a one-time medical bill. It’s an ongoing expense that can last for years—sometimes even decades.

These figures don’t include incidental costs like medical equipment, transportation, or caregiver burnout. The financial strain on families can be overwhelming.

Read more: Singlife Careshield Review

Read more: How pre-exisiting medical conditions can affect your insurance applications

Do you know: You can use up to $600 per year from your Medisave for your private add-on Careshield Premiums. Enjoy coverage without using cash today! Whatsapp us today to find out how much you can be covered with your $600 medisave budget!

📉 Most Singaporeans Still Aren’t Covered

Despite government initiatives like ElderShield and CareShield Life, many Singaporeans remain underinsured or unaware of what’s covered.

Here’s the current situation:

CareShield Life is mandatory only for Singaporeans born in 1980 or later, unless older residents opt in.

Monthly payouts (as of 2025) start at $649/month, which may not be sufficient to fully cover care costs.

A large proportion of older Singaporeans either aren’t enrolled or haven’t supplemented their plans.

📊 Shocking but True:

1 in 2 Singaporeans aged 65 today will become severely disabled in their lifetime.

Less than 30% of older adults have long-term care insurance beyond the basic government schemes.

Many falsely believe MediSave or MediShield Life covers long-term care needs—it doesn’t.

Singlife recently released a white paper urging action on Long Term Care, you can read more about it here.

😟 Why the Coverage Gap?

Several reasons explain this widespread under-preparedness:

Low awareness of what CareShield Life actually provides.

Misconceptions about other healthcare schemes covering long-term care.

Procrastination—many only act after a disabling event strikes.

Cost concerns about insurance premiums, especially for older individuals.

🛡️ Bridging the Gap: What You Can Do

Being financially prepared for long-term care is possible—but only with early action. Here are steps to take now:

✅ Check your CareShield Life status – Are you enrolled? Are the payouts enough?

- How to check whether do you have Careshield Life?

- Login to CPF website using your Singpass, navigate to ‘My Dashboard’ and select ‘Healthcare’. Lastly, locate and click on the “Long-term care insurance” section to view your CareShield Life coverage details.

- How to check whether do you have Careshield Life?

🔍 Explore CareShield Life supplements – Top up your coverage with private insurers to receive higher monthly payouts. You can use up to $600 per year from your Medisave to get extra long term care coverage!

💬 Speak with a financial advisor – They can help assess your risks and tailor a protection plan.

📅 Start early – Premiums are lower and coverage is higher when you begin young and healthy.

🧠 Final Thoughts

Singapore’s long-term care system is evolving—but for now, basic coverage often falls short of real-life costs. As life expectancy rises, so do the chances of needing long-term care. Don’t wait for a crisis. Plan ahead—because the cost of doing nothing could be far greater.

👉 Contact us today for a free, no-obligation consultation. Let’s walk you through it—no cost, no pressure. Leave your contact details via the form below or Whatsapp us today!