When it comes to protecting yourself against rising healthcare costs in Singapore, many wonder: Which is the best Integrated Shield Plan (ISP) in 2026? With multiple insurers offering MOH-approved Integrated Shield Plans (and different rider designs), choosing the right medical insurance can feel overwhelming.

In this guide, we compare MOH-approved Integrated Shield Plans and riders across insurers, looking at premiums, benefits, coverage differences, and rider trade-offs, so you can decide what fits your budget, preferred hospital class (B1/A/Private), and comfort level with out-of-pocket costs.

Last updated: 20 Feb 2026 (coverage features, rider framework changes, and MOH guidance reviewed).

2026 Important Update: ISP Rider Rules Change from 1 April 2026

Starting 1 April 2026, new Integrated Shield Plan riders sold in Singapore must follow revised MOH requirements. In plain English: even if you buy a rider, your guaranteed out-of-pocket cost can be higher than before, because riders can no longer “wipe out” the deductible portion completely.

What’s changing (from 1 Apr 2026):

Riders can no longer cover the minimum ISP deductible set by MOH (you’ll need to pay at least the deductible amount before coverage kicks in).

The minimum co-payment cap increases to S$6,000/year (up from the previous minimum of S$3,000). This cap applies to co-payments excluding the minimum deductible.

The minimum 5% co-payment requirement remains.

Who this affects:

Buying a new rider from April 2026 onward: expect riders to be structured with higher cost-sharing than the older “full deductible cover” style.

Buying an older rider before 1 April 2026: insurers can sell existing riders until 31 March 2026, but buyers during this period must be told they’ll transition to a compliant rider no later than the next renewal after 1 April 2028.

Why it matters for “best ISP 2026”: from April 2026, the “best” choice isn’t just about claim limits, it’s also about how much certainty you want over out-of-pocket costs, and whether you’re comfortable following panel doctor conditions to maximise rider benefits.

What Is an Integrated Shield Plan (ISP) in Singapore?

An Integrated Shield Plan is a private medical insurance policy that supplements MediShield Life. It provides higher coverage limits and lets you choose treatment at A ward, B1 ward, or private hospitals.

Key features of ISPs in Singapore include:

Higher annual claim limits (some over $1 million in 2026)

Options for private or restructured hospital coverage

Optional riders to reduce co-payment or out-of-pocket costs

Premiums payable partly with CPF MediSave

MediShield Life vs Integrated Shield Plans (ISP): What’s the Real Difference?

Many Singaporeans ask: “Is MediShield Life enough?” The honest answer is: it depends on where you want to be treated and how much out-of-pocket certainty you want when a hospital bill happens.

MediShield Life (Basic, universal coverage)

MediShield Life is the national basic health insurance plan. It provides coverage mainly geared towards subsidised treatment in public hospitals and comes with claim limits and cost-sharing that are designed to keep premiums affordable for everyone.

Best for: those who are comfortable with subsidised wards, and want basic protection for large bills.

Integrated Shield Plan (Enhanced coverage on top of MediShield Life)

An Integrated Shield Plan (ISP) is private insurance that supplements MediShield Life, giving you higher coverage and allowing you to insure for:

B1 / A wards in public hospitals, and/or

Private hospitals (depending on the plan tier you choose)

Best for: those who want higher claim limits, more choice of ward/hospital, and stronger protection against large private hospital bills.

What About Riders? Do They Still “Reduce My Bill to Almost Nothing” in 2026?

Riders still help, but it’s important to understand the 2026 shift:

A rider can reduce your share of the bill through co-payment caps (and sometimes better benefits if you use panel doctors).

From 1 April 2026, new riders cannot cover the minimum ISP deductible set by MOH, and the minimum annual co-payment cap for new riders increases to S$6,000 (cap applies to co-payments, excluding the minimum deductible).

What this means in plain English:

Even with a rider, you should expect a higher minimum out-of-pocket “floor” than older riders that could cover deductibles more fully. But for big bills (especially private hospital bills), riders still matter because they can prevent your share from ballooning beyond the cap structure.

Why This Matters (Realistic Bill Example)

Healthcare costs are rising, and private hospital bills can add up quickly. For instance, a short private hospital stay for a common condition can already run into a few thousand dollars, depending on the hospital, doctor fees, tests and medications. That’s why many people choose an ISP tier that matches where they want to be treated.

For rough cost references, MOH publishes Hospital Bills and Fee Benchmarks for private sector doctor and hospital fee ranges, which you can use as a guide when estimating typical bills.

Quick Rule of Thumb (How to Decide)

Choose MediShield Life only if:

You’re comfortable with subsidised treatment and want basic protection.

Consider an Integrated Shield Plan if:

You want B1/A ward or private hospital options,

You value higher claim limits, and

You want more predictability for large bills (especially with a rider, while remembering the 2026 rider framework change).

Key Differences Between ISP Riders in Singapore (2026 Update)

Your Integrated Shield Plan (ISP) covers large hospital bills, but the rider determines how predictable your out-of-pocket cost will be, especially if you prefer private hospitals or want a smoother claims experience.

1) Riders reduce your share of the bill, but 2026 rules raise the minimum you must pay

In the past, many riders were positioned as “very low cash outlay” (e.g., 5% co-pay). From 2026 onward, it’s more important to understand what a rider cannot cover.

2026 note (new riders sold from 1 Apr 2026): riders can’t cover the MOH minimum ISP deductible, and the minimum annual co-payment cap is S$6,000 (cap applies to co-payments, excluding the deductible). The minimum 5% co-payment requirement remains.

What this means in plain English: even with a rider, you should expect a higher minimum out-of-pocket “floor” than older riders that could cover deductibles more fully — but riders still protect you from very large bills by limiting how high your co-payments can climb.

Tip: When comparing riders in 2026, don’t just look at “5%.” Compare (a) deductible treatment, (b) co-payment cap, and (c) panel rules.

2) Co-payment structure: 5% vs 10% (why the cap matters more than the %)

Most riders require you to pay a portion of the bill (commonly 5% or 10%) and then cap that amount per policy year.

Lower % (e.g., 5%) usually feels safer for large bills, but premiums may be higher.

Higher % (e.g., 10%) may be cheaper, but your share grows faster until you hit the cap.

When comparing riders, check:

Co-payment %

Annual co-payment cap

Whether cap terms change for panel vs non-panel

What is included/excluded (some items may be outside rider benefits depending on product rules)

3) Panel vs Non-panel doctors

Most riders are designed to encourage panel usage. This affects both:

How much you pay, and

Whether claims are smoother (e.g., pre-authorisation / LOG / preferred fee arrangements).

A common pattern is:

Panel / pre-authorised → lower out-of-pocket, better caps, better process

Non-panel → higher out-of-pocket, reduced benefits, or stricter claim conditions

If you prefer private specialists (e.g., Mount E / Gleneagles / Parkway networks), panel breadth matters, a “cheap rider” can become expensive if you frequently use non-panel doctors.

4) Pre- and post-hospitalisation coverage (watch the days + what’s included)

Insurers differ on:

Pre-hospitalisation: commonly 90 to 180 days

Post-hospitalisation: commonly 180 to 365 days

This matters for conditions that need repeated consults, scans, and follow-ups. Also check what counts as post-hospitalisation (e.g., rehab/TCM follow-ups can vary by insurer/product).

5) Cancer drug treatment (CDL vs non-CDL): still a major comparison point

A key difference between plans/riders is coverage for:

Treatments on the Cancer Drug List (CDL)

Treatments not on the CDL (often a monthly cap)

When comparing, include:

CDL multiple (relative to MediShield Life)

Non-CDL monthly cap

Pre-authorisation requirements and panel restrictions

How to choose the right rider in 2026 (simple guide)

Choose a rider that prioritises lower out-of-pocket uncertainty if you:

Prefer private hospital access

Want predictable cost-sharing for large bills

Are comfortable using panel specialists for stronger rider protection

Choose a rider that prioritises affordability if you:

Mainly want catastrophic bill protection

Can accept higher co-pay as long as there’s a cap

Want premiums to remain sustainable long-term

Most important in 2026: compare riders based on deductible + co-pay cap + panel conditions, not just marketing labels.

Example (2026): How your out-of-pocket is calculated, with deductible + co-pay + cap

Illustration only (for easy reference):

Assume your plan has a deductible of S$3,500 and your rider has 5% co-payment, with an annual co-payment cap of S$6,000.

In 2026, new riders can’t cover the MOH minimum deductible, and the co-payment cap applies to co-payments (excluding deductible).

Example 1: S$20,000 hospital bill

Pay deductible first: S$3,500

Remaining bill after deductible: S$20,000 − S$3,500 = S$16,500

Co-payment (5%) on remaining: 5% × S$16,500 = S$825

Check cap: S$825 is below S$6,000, so no capping needed.

✅ Estimated out-of-pocket = S$3,500 + S$825 = S$4,325

Example 2: S$200,000 hospital bill (shows why the cap matters)

Pay deductible first: S$3,500

Remaining bill after deductible: S$200,000 − S$3,500 = S$196,500

Co-payment (5%) on remaining: 5% × S$196,500 = S$9,825

Apply co-payment cap: co-pay is capped at S$6,000

✅ Estimated out-of-pocket = S$3,500 + S$6,000 = S$9,500

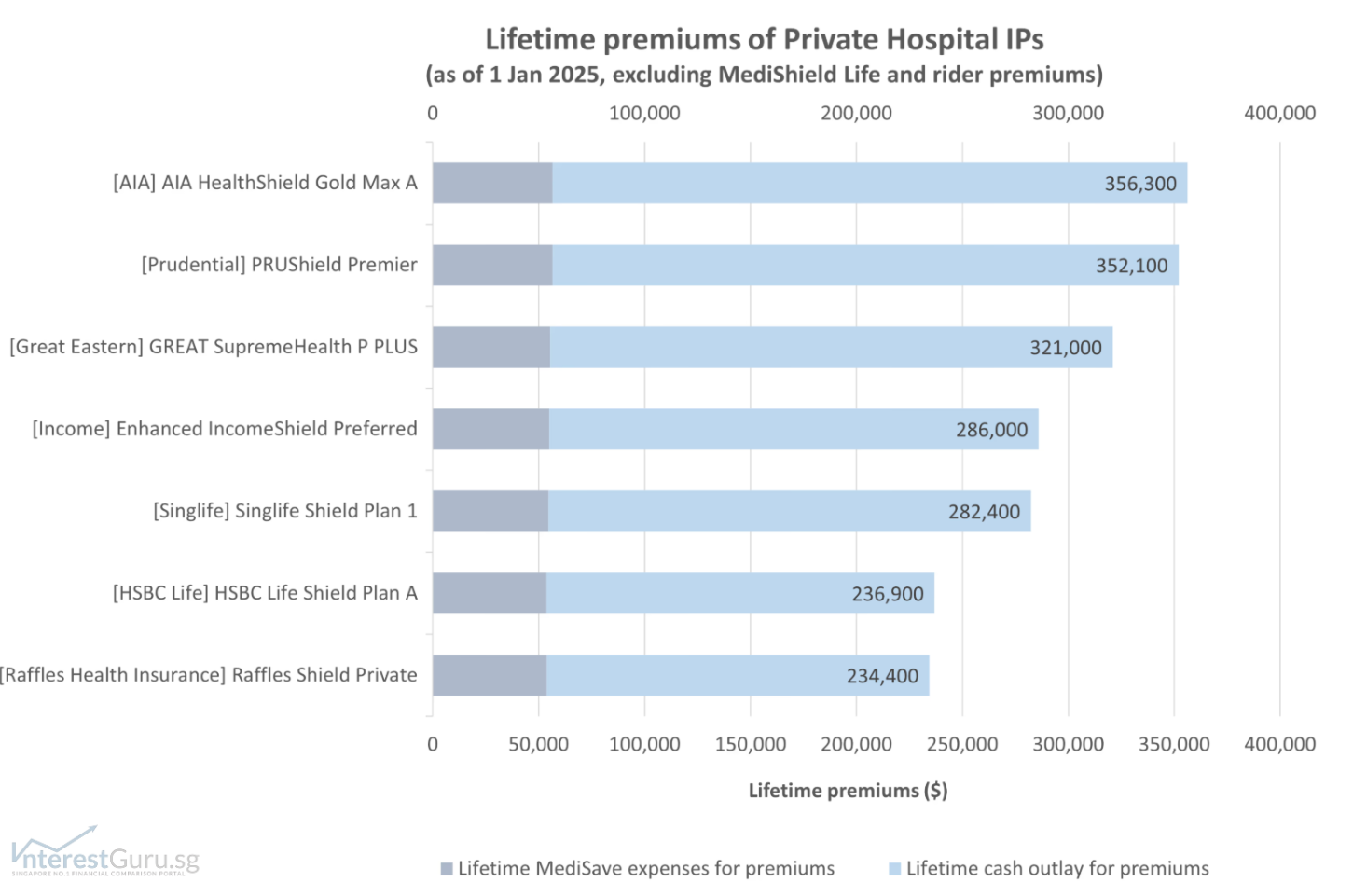

Lifetime Premiums Comparison for Private Hospital ISPs

The Ministry of Health (MOH) has previously published a lifetime premium comparison for private hospital Integrated Shield Plans across major insurers. This is helpful for seeing which plans tend to be more affordable over the long run, but do note that lifetime premiums can change with repricing, and the table typically excludes MediShield Life and rider premiums.

How to use this table: Treat it as a directional guide for long-term affordability. Always confirm your exact premium (based on age next birthday and plan tier) before deciding.

How We Ranked the Best Integrated Shield Plans in 2026

To shortlist the best ISPs in Singapore for 2026, we focused on 7 practical factors that affect claims and out-of-pocket costs:

Plan tier: Public (A/B1) vs Private hospital

Annual / policy year limit (catastrophic bill protection)

Pre- and post-hospitalisation coverage (days + what’s included)

Cancer drug coverage (CDL and non-CDL monthly limits)

Rider cost-sharing: deductible + co-payment + annual cap (post–1 Apr 2026 framework)

Panel strength & penalties (what happens if you go non-panel)

Claims experience: LOG, pre-authorisation, service network

Based on the criteria above, Interestguru.sg shortlisted three options that offer strong value in different situations: overall coverage, affordability, and family suitability.

Updated for 2026: This shortlist considers the rider framework effective 1 April 2026, which impacts how much riders can reduce your minimum out-of-pocket.

- Best Integrated Shield Plan/ Rider for overall coverage – HSBC Life Shield and HSBC Life Enhanced Care

- Best Integrated Shield Plan/ Rider for affordability – NTUC Income Enhanced IncomeShield and NTUC Income Classic Care Rider

- Best Integrated Shield Plan/ Rider for entire family coverage – Singlife Shield and Singlife Health Plus

HSBC Life Shield and HSBC Life Enhanced Cover – Best for Overall Coverage

Who it suits: You want strong private hospital protection with a straightforward rider design, and you value smoother claims support.

Highlights

High policy year limit: $2.5 million per year

Strong pre/post coverage: 180 days pre-hospitalisation, 365 days post-hospitalisation

Outpatient benefits: fractures, dislocations, sports injuries, dengue fever. hand, foot & mouth disease and food poisoning

Strong cancer drug coverage: 23x of Medishield Life’s claim limit

$15,000/month coverage for cancer treatment not on CDL

LOG / pre-assessment support: 24 hour support, 3 working days

No claim discount: up to 20%

GP and Specialist preferred consultation fees under panel healthcare providers

Planned overseas medical treatment: Up to $50,000

Watch-outs

Panel rules matter for best rider benefits

Premiums vary significantly by age, check your exact quote

Bottom line: Strong “overall package” if you want coverage depth + claims convenience.

Read about: HSBC Life Shield

Read about: HSBC Life Enhanced Care

NTUC Income Enhanced IncomeShield and NTUC Income Classic Care Rider – Best for Affordability

Who it suits: You want private hospital protection with a lower ongoing premium, and you’re okay with a simpler “essentials-first” feature set.

Rider choice (simple):

Policy year limit: $1.5 million per year

Classic Care Rider: higher co-pay % than Deluxe, but still capped annually → tends to be better value for many budget-focused buyers

Deluxe Care Rider: lower co-pay %, higher premium → suits those who want lower bill share upfront

Strong pre/post coverage: 180 days pre-hospitalisation, 365 days post-hospitalisation

Strong cancer drug coverage: 23x of Medishield Life’s claim limit

$15,000/month coverage for cancer treatment not on CDL

Watch-outs

No planned overseas treatment

Fewer “extras” like outpatient benefits

Bottom line: One of the most cost-efficient ways to maintain private hospital coverage without overpaying.

Read about: NTUC Income Enhanced Incomeshield

Singlife Shield and Singlife Health Plus – Best for Entire Family Coverage

Who it suits: Families who want to optimise coverage across spouse + children, especially if you value family-specific perks.

Highlights

Family/child coverage feature: Discounted premium rates under plan 2, if both parents are covered under Singlife Shield Plan 1 or 2. Up to 4 children, till age 20

Policy year limit: $2 million per year

Strong pre/post coverage: 180 days pre-hospitalisation, 365 days post-hospitalisation

Cancer drug coverage: 20x of Medishield Life’s claim limit

$15,000/month coverage for cancer treatment not on CDL

Lump-sum payout of S$10,000 for critical illnesses per lifetime

- Letter of Guarantee (LOG) waives up to S$80,000 of hospital admission deposit

Watch-outs

Rider terms differ (Prime vs Lite)

Panel conditions affect out-of-pocket

Bottom line: Great family proposition if you qualify for the child coverage structure and you’ll use the benefits.

Read about: Singlife Shield

Read about: Singlife Health Plus

Thinking of Switching to Another Integrated Shield Plan?

Switching ISPs can make sense if you’re healthy and premiums have become less competitive, but it’s not always straightforward.

If you have pre-existing conditions, the new insurer may apply exclusions, loading, or decline the rider application.

Even if your base ISP can be approved, the rider is often harder to obtain if there are medical disclosures.

If affordability is the concern, consider downgrading plan tier (e.g., Private → A ward) within your existing insurer, which is usually simpler than switching.

Read more: How Pre-exisiting Medical Conditions can affect your insurance application

Frequently Asked Questions (FAQ)

1) What changed for ISP riders in April 2026?

From 1 April 2026, new riders must follow updated MOH requirements including that riders can’t cover the MOH minimum deductible, and the minimum annual co-payment cap for new riders is S$6,000 (excluding deductible). This means riders still help, but the minimum out-of-pocket “floor” is higher than some older rider designs.

2) Which is the cheapest Integrated Shield Plan in Singapore (2026)?

It depends on your age next birthday and the plan tier (Public A/B1 vs Private). A good strategy many people use is to start with the tier you want (often Private), and if premiums become unaffordable later, consider a downgrade.

3) Can I pay for Integrated Shield Plans using CPF MediSave?

Yes, up to the MediSave Additional Withdrawal Limits (AWL) based on age. Any excess premium must be paid in cash.

4) Do I need an Integrated Shield Plan if I already have MediShield Life?

If you want A/B1 wards or private hospitals, an ISP provides higher claim limits and more protection against large bills compared to MediShield Life alone.

5) Are ISP riders worth it in 2026?

Often yes, especially for private hospital users, because riders can cap your co-payments and reduce bill uncertainty. But in 2026, compare riders based on deductible + co-pay cap + panel conditions, not just “5%”.

Which is the best Integrated Shield Plan for you?