In general, Money in CPF Accounts cannot be withdrawn for personal use. The funds in your CPF-OA and CPF-SA will be transferred to the Retirement Account at Age 55.

Upon reaching Age 65, you will be entitled to a lifelong monthly payout through CPF LIFE.

Currently, there are three CPF LIFE Scheme options: LIFE Standard Plan, LIFE Basic Plan or LIFE Escalating Plan (CPF LIFE, Open in new window).

What else can I do with my CPF monies?

Besides paying for your property, the government allows the use of CPF funds for individual looking to enhance their retirement income, seeking higher education or getting hospitation and medical coverage. Check out 5 ways you can make use of your CPF account below:

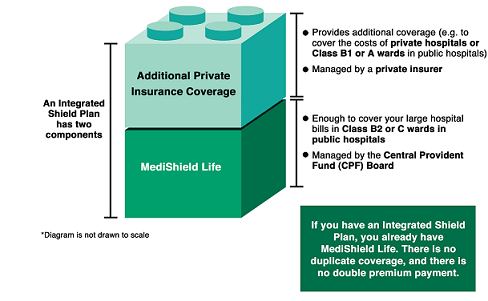

Insurance – Get Hospitalisation and medical coverage

Medishield Life will cover your basic hospitalisation needs in a Class B2/ C government hospital ward. However, it may not be enough to cover hospitalisation and medical expenses for private and stay in higher class wards as the medical expense are not as heavily subsidised compared to B2/ C ward charges.

An Integrated Shield Plan is a must for everyone as it greatly reduces or fully covers the cost of hospitalisation. It allows you to stay in private, Ward A or Ward B1 with no shocking bills upon discharge.

Whatever else not covered by Integrated Shield Plan can be enhanced by getting an add-on rider using cash, which fully covers the cost of co-insurance and deductible.

Read about: 5 Reasons why upgrading your MediShield Life is a TOP PRIORITY

For most age band until age 70 and onwards, little or no additional cash is required. Using your Medisave to purchase an Integrated Shield Plan allows the remaining funds in your Medisave account to earn a 4% p.a. return while your hospitalisation bills are covered.

Learn more about Integrated Shield Plan with our FAQs on MediShield upgrades.

Compare integrated shield plans benefits and coverages with our compareNow feature!

Personal development – Upgrade your education/ skills set

Upgrading of personal skill set and profession education increases employability and allows one to stay relevant to the needs of the workforce. As long as the diploma or degree is from a CPF Approved Educational Institutions (AEIs), you could be better off paying for it using your CPF-OA.

Compare this to a bank loan, which will typically charge anywhere from 4% to 6% p.a. interest. It is granted that you have to start making payments one year after completion of your studies with accrued interest (based on how much the money would have grown had it stay in your CPF-OA).

At the end of the day, the money and interest you repay still go back to your CPF-OA account, as compared to interest paid towards the bank.

Investments – Accumulate wealth for retirement

Depending on the amount of risk you are willing to take, CPF-OA, CPF-SA and even SRS (if you have done voluntary top-up) can be used to enhance return via instruments such as Exchange Traded Funds (ETFs), Unit Trust Funds, Single Premium Insurance, investment-linked policies or life annuities.

As CPF-OA balance above the first S$20,00 earns only 2.5% p.a. interest, CPF board allows investment on remaining balance above S$20,000 for investment purposes.

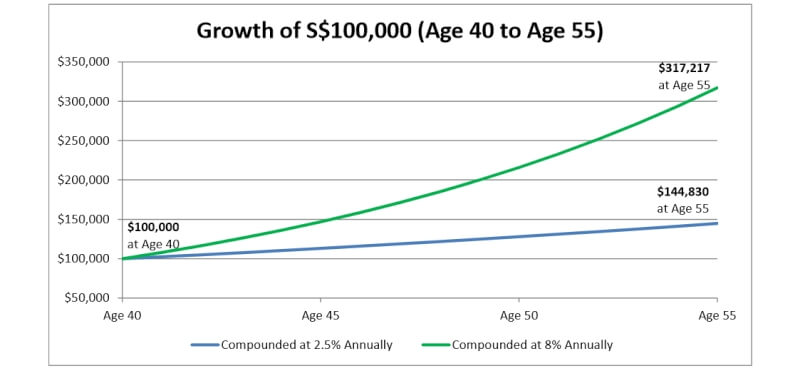

Assuming an average long-term growth of 8% returns on your CPF funds, this is what a S$100,000 investment will be by the time you turn 55:

While not principle guaranteed, long-term investment in a managed unit trust fund may potentially return compounded yields upward of 8% p.a. or even higher, allowing a higher amount of monthly income when your CPF-OA funds switch to your CPF Retirement Account at Age 55.

Refer to our various investment articles for more about Unit Trust Funds.

Get higher interest – Transfer to CPF Special account (CPF-SA)

There are advantages and disadvantages of transferring from CPF-OA to CPF-SA. CPF-OA funds earn an interest of 2.5% p.a. interest and can be used for the purchase of a property. Once transferred to CPF-SA, the fund cannot be switched back to CPF-OA.

Notwithstanding any changes by the CPF Board, CPF-SA allows earning a relatively “risk-free” 4% p.a. interest on their funds.

This will be attractive to conservative individuals that do not wish to have any investment risk or price volatility on their CPF funds. However, note that there are more restrictions on what you can do with your CFP-SA account, including the choices of CPF investments.

Read about: Why you should plan for your retirement now

Get Tax Relief – by topping up to SRS account

By voluntary topping up cash to SRS account, you can also get a tax rebate on your payable income tax. For individuals that barely just passed to a higher tax bracket, the top-up amount may result in a lower tax bracket. You end paying lesser income tax and have a higher monthly income upon retirement from your CPF LIFE.

As SRS account interest rates are significantly lower, there are approved SRS unit trust funds that can potentially enhance return on the funds sitting on your SRS account.

Alternatively, the risk adverse individuals can consider taking up an annuity or retirement plan.

Need to know more about using CPF to get insurance coverage or your investment options?

Drop us a message to us and let InterestGuru.sg assign an licensed financial adviser to answer your questions. Alternatively, use our compareNOW to get the 3 best quotes for all insurance and investment products and services across insurance companies in Singapore.

Learn something valuable today?

You can thank us by simply liking our facebook page and sharing this post with the people you love ?

Distribution policy: This article, its contents and information stated here may be partially or completely reproduced as long as proper credit and backlinks are attributed back to the main site at InterestGuru.sg.