The finer details on what makes the newly launched MyWholeLifePlan II from Aviva unique among the pool of whole life insurance policies in Singapore.

*Early Disclaimer* At InterestGuru.sg, we do not take any remuneration or incentive in any form or method from any of the insurers. Exceptional cases are made for outstanding products to remain a neutral financial comparison portal.

NOTE: Aviva MyWholeLifePlan II has been discontinued and replaced by Aviva MyWholeLifePlan III.

Related article: How much insurance coverage do you need? *NEW*

Why do multiple claims for Early Critical Illness and Critical Illness matters?

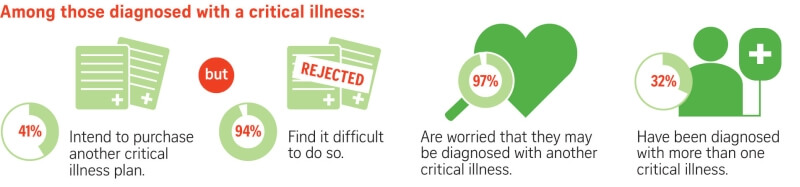

Anyone that had contracted any form of Critical Illnesses would have known the importance of insurance coverage. It is no surprise that the same group of individuals would wish to get coverage for Critical Illness. But should you wait until you diagnosed with a critical illness before getting insurance coverage?

Here are some quick stats from the AIA Health Matters Survey 2016 published in The Straits Times as below:

While relapse of cancer or getting other critical illness is heard of, getting insurance coverage is usually impossible or with heavy exclusion clauses.

Aviva MyWholeLifePlan II is featured in our 8 Best Whole Life Insurance Plans in Singapore for best in Optional Insurance Riders/ Highest Surrender Value features. *NEW*

Why makes Aviva MyWholeLifePlan II unique?

The base plan of MyWholeLifePlan II

The base plan of Aviva MyWholeLifePlan II by itself is nothing special with up to 4 times coverage multiplier on the Sum Assured value. For the records, Manulife LifeReady offers coverage multiplier up to 5 times of the Sum Assured at a similarly competitive premium.

Hence, there is nothing to shout about if all you are looking for in a whole life plan is coverage for Death, Disability or Terminal Illness.

The available riders of MyWholeLifePlan II

Almost all whole life plans in the markets allow for additional riders to cover Critical Illness and Early Critical Illness. The riders will expire upon making a payout, and there is no further need to pay the insurance premium for the rider as well.

You then wonder how you are going to get insurance coverage under existing medical conditions.

Now, this is where Aviva MyWholeLifePlan II stands out among all the whole life insurance plans. As the name suggests, the MultiPay Critical Illness Cover II rider allows multiple claims on the chosen Sum Assured value.

How does the MultiPay Critical Illness Cover II rider work?

Here is how the MultiPay Critical Illness Cover II works when you take the rider with a Sum Assured of S$50,000:

- 1st Layer – Early/ Intermediate Stage Critical Illness ( Allows claim for 2 times, each claim at 1x of Sum Assured)

- 2nd Layer – Critical Illness (Allows a total payout of up to 3x Sum Assured for a total of S$150,000 less amount paid in the 1st Layer, minimally you get 1x of Sum Assured at S$50,000 if S$100,000 was paid out earlier).

At this stage of the claim, future premium for MultiPay Critical Illness Cover II is waived. There will be 2 years waiting period before further claims are allowed.

- 3rd Layer – First time CI or Relapse CI (Allows claim for 1x of Sum Assured at S$50,000)

- First time CI: Major Cancer, Heart Attack or Stroke

- Relapse CI: Re-diagnosed Major Cancer, Recurrent Heart Attack or Recurrent Stroke

There will be another 2 years waiting period before further claims are allowed.

- 4th Layer – First time CI or Relapse CI (Allows claim for 1x of Sum Assured at S$50,000)

- First time CI: Major Cancer, Heart Attack or Stroke

- Relapse CI: Re-diagnosed Major Cancer, Recurrent Heart Attack or Recurrent Stroke

In short, the rider can pay up to 5 times the Sum Assured of your chosen amount. Don’t be shy if you are confused, it took us a while to fully understand how it works.

Feel free to drop us a message, if you are looking at coverage for multiple claims.

How can you get coverage for multiple Critical Illness?

Insurance payout for multiple critical illnesses in a single insurance plan or rider is a relatively new offering across Singapore insurers. Such coverages are usually added on as a rider to a term or whole life plan. or as a stand-alone critical illness plan.

Coverage via Term Insurance/ Multiple Critical Illness Plans

As a stand-alone policy or rider in a term insurance plan, you can look into Aviva My MultiPay Critical Illness Plan, AIA Triple Critical Cover or Great Eastern Critical Care Advantage.

The overall premium will be lower compared to a whole life plan as the policy does not accumulate cash value. Similarly, a term or critical illness plan will terminate/ expire at the end of your chosen coverage term, even if there was no payout made.

Read about: Which is Better – Term Life Plan or Whole Life Plan?

Coverage via riders in a Whole Life Plan

If life-long coverage and accumulation of cash value was your objective, multiple critical illness coverages can only be added on as a rider in the newly launched Aviva MyWholeLifePlan II. It is a no-brainer that MyWholeLifePlan II should be the first on your consideration list if whole life plan was your intention.

As of 22/1/2023, Aviva MyWholeLifePlan II the only whole life plan with multiple critical illness payouts.

Alternatively, look at our in-depth review of the 3 Best Whole Life Plans in Singapore for Insurance Coverage (2023 Edition)

Find out more about whole life insurance plans

Wish to know more about how a whole life insurance policy fit into your financial and insurance portfolio? Like to know the actual financial returns on the above products based on your age, budget and financial profile?

Get INSTANT QUOTES and detailed information based on your individual profile using our whole life plan selector now!

Compare and get your personal proposal for insurance coverages

Our licensed financial adviser will draft their recommendations and proposals based on your given input. Your information and details will only be used for communication with you. All comparisons done are solely based on your individual needs.

We compare whole life quotations on all leading insurers in Singapore

Too much work to fill in the form above?

Alternatively, use our CompareNOW to compare whole life insurance policies across insurance companies. Compare and get the best for yourself, it doesn’t have to cost you!

Have a burning question about your insurance coverages?

Drop us a message to us and let InterestGuru.sg assign an licensed financial adviser to answer your questions. Alternatively, use our compareNOW to get the 3 best quotes for all insurance and investment products and services across insurance companies in Singapore.

Learn something valuable today?

You can thank us by simply liking our facebook page and sharing this post with the people you love ?

Distribution policy: This article, its contents and information stated here may be partially or completely reproduced as long as proper credit and backlinks are attributed back to the main site at InterestGuru.sg.