Table of Contents – Best Retirement Plans in Singapore

- 1 What makes a good retirement plan or annuity policy?

- 2 Why do you need a retirement plan?

- 3 The best retirement plans based on features and income payout

- 3.1 Best High Income Retirement Plan for Guaranteed Payout – Manulife RetireReady Plus III

- 3.2 Best High Income Retirement Plan for Disability Payout – NTUC Income Gro Retire Flex

- 3.3 Best High Income Retirement Plan for Projected Payout – Singlife Flexi Retirement

- 3.4 Best High Income Retirement Plan For Lump-sum Payout – AXA Retire Treasure II

- 4 Detailed comparison for retirement plans based on features and income payout

- 5 How do you get the most out of your retirement plan?

- 6 What are the other alternatives besides a high income retirement plan?

- 7 What are the best retirement annuity plans for you?

- 8 Find the best retirement plans and annuity policies with the highest income payout here!

- 9 Frequently Asked Questions (FAQs)

Retirement plans or annuities, when paired together with your lifelong payout from your CPF LIFE, can supplement your retirement income during your golden years. You can even expect a payout multiplier (2x) due to disability or when you are unable to perform a minimum 2 or 3 of 6 ADLs.

As you will be committing a significant portion of your life savings, ensure that the payout for your retirement plan is competitive and personalised to your needs.

For this comprehensive review, InterestGuru.sg looks into the best retirement plans in Singapore that provide the highest income payout toward meeting your lifestyle needs and expenses.

- Best High Income Retirement Plan for Guaranteed Payout – Manulife RetireReady Plus III

- Best High Income Retirement Plan for Disability Payout – NTUC Income Gro Retire Flex

- Best High Income Retirement Plan for Projected Payout – Singlife Flexi Retirement

- Best High Income Retirement Plan for Lump-sum Maturity Payout – AXA Retire Treasure II

Related article: The Complete Guide to Retirement Planning (2023 Edition) *NEW*

What makes a good retirement plan or annuity policy?

The main objective of a retirement plan or annuity policy would be to provide a consistent stream of income starting from your preferred retirement age. Ideally, a shorter premium tenor would provide the highest yield to the maturity of the policy.

In order to retire without much financial stress, you should look to increase the number of income streams you have. This will guard you against the event where one income stream runs dry.

A retirement annuity plan helps you to achieve that by paying out guaranteed monthly income as well as potential bonuses upon reaching your chosen retirement age. In this post, we breakdown what are some of the best retirement plans offered in Singapore and which fit your unique needs.

Depending on individual retirement plans, additional options may even be available to further optimize your overall financial yields.

Our pick for the 4 Best Retirement Plans and Annuities in Features and Income Payout are based on the criteria below:

- Policy options available for premium tenor

- Policy options available for the period of income payout

- The rate of financial returns and payout (Guaranteed and Non-Guaranteed)

- Choice and features of riders to complement health coverage (Additional guaranteed payout)

- Product features unique to the listed retirement plans

Looking for a retirement plan that fits your needs and budget? Head over to InterestGuru’s Retirement Plan Compare Portal to compare retirement plans and annuity policies across insurers.

Read also: 3 things to consider before taking up a new financial product

Read also: 8 commonly made financial mistakes in Singapore

With all insurance companies in Singapore offering their own retirement plans, make sure you select only the best for yourself!

Why do you need a retirement plan?

Your CPF LIFE payout will supplement your income during your retirement and assist with your basic living needs. However, it will not be realistic to expect CPF Life to provide a high level of comfort for your lifestyle.

Consider the following questions:

- Are you looking to still have a high and stable income despite a lower workload as you ages?

- Are you still preparing your financials to sustain your lifestyle when you stop working?

- Is maintaining a specific lifestyle important even as daily costs go up?

- Does your ideal retirement lifestyle involve discretionary spending such as frequent overseas travelling?

- Are stability and predictability what you seek in a financial product when it comes to your income stream during your retirement years?

If your answer to the above questions is mostly yes, you may wish to consider taking up a retirement plan for a constant stream of income.

Basics of retirement planning: How does a retirement plan work?

Basics of retirement planning: When should you start saving for your retirement?

The best retirement plans based on features and income payout

In no order of preferences or ranking, we present the best retirement plans that offer a stream of the highest income payout to meet your retirement needs.

As your retirement goals and objectives are unique based on your individual expectation, ensure that your retirement plan is customised to fit your lifestyle needs.

Best High Income Retirement Plan for Projected Payout – Manulife RetireReady Plus III

Manulife RetireReady Plus III is a retirement income plan that gives you the flexibility to choose:

- Your desired retirement age at 55. 60, 65 or 70 years old

- Income payout period of up to 80, or up to 90 or for a lifetime

- Your desired amount of monthly guaranteed income

- Your desired premium payment term of 5, 10, 20 years or single premium (SRS option available)

What’s NEW in Manulife RetireReady Plus III:

- Retrenchment benefit is now 50% of your annual premium (up from 40% with RetireReady Plus II)

RetireReady Plus III will be 100% principal guaranteed upon retirement age and comes with Loss of Independence Benefits which is equivalent to your monthly guaranteed income payable should you not be able to perform 3 out of 6 Activities of Daily Living (ADLs).

Should you be unable to perform at least 2 of 6 ADLs, the monthly guaranteed income payable will still be increased by 50%. RetireReady Plus III is also a hassle-free application. There is no need for health underwriting and it also provides a premium waiver should you be disabled during the premium payment period.

It is also worth noting that the revised projected return rate is now 3% and 4.25% from previously 3.25% and 4.75% respectively.

What we like about Manulife RetireReady Plus III

- Single premium option available

- You can choose to pay your premiums using cash or CPF SRS account

- Income payout period can go as long as for life

- 100% principal guaranteed upon reaching retirement age

- No health underwriting needed

- Option to receive a non-guaranteed bonus in a lump sum or spread it into your monthly income at retirement age

- 1.5X of Monthly Guaranteed Income – Upon unable to perform 2 out of 6 ADLs

- 2X of Monthly Guaranteed Income – Upon unable to perform 3 out of 6 ADLs

- Retrenchment benefit the sum of 50% your yearly premium

What we do not like about Manulife RetireReady Plus III

- Retirement age is fixed in blocks of 5 years starting from 55 years old. Policyholders could not choose retirement age below 55 years old, or choose to retire at a specific age.

More about: Manulife RetireReady Plus III (The complete policy review)

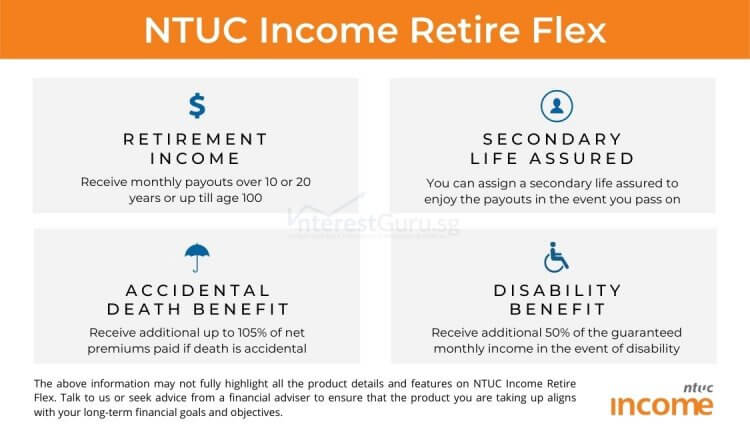

Best High Income Retirement Plan for Guaranteed Payout – NTUC Income Gro Retire Flex

Gro Retire Flex by NTUC Income offers an overall high guaranteed and projected monthly income payout. Compare to its peers, Disability Care Benefit offers the best coverage for disability and multiplied income.

NTUC Income Gro Retire Flex gives you the option to choose:

- Your preferred retirement age

- Your preferred amount of monthly guaranteed income

- Your preferred number of years (10 or 20 years, or up till age 100) to receive your monthly payout

- Your preferred premium term (Single premium; Cash or SRS, 5 to 30 years; 5 year increments)

- Hassle-free application – No health underwriting needed

Unlike the definition of Total and Permanent Disability (TPD) or LOI (Letter of Indemnity), NTUC Income Disability Care Benefit is valid with any one of the following

- Loss of use of one limb

- Loss of speech or hearing

- Loss of sight in one eye due to accidental injury or illness

Disability before payout starts not only waives all future premiums but provides an additional guaranteed lump sum benefit, equivalent to six times the monthly cash benefit.

Related article: 5 reasons you should invest in a retirement annuity plan

In-depth financial details for NTUC Income Gro Retire Flex

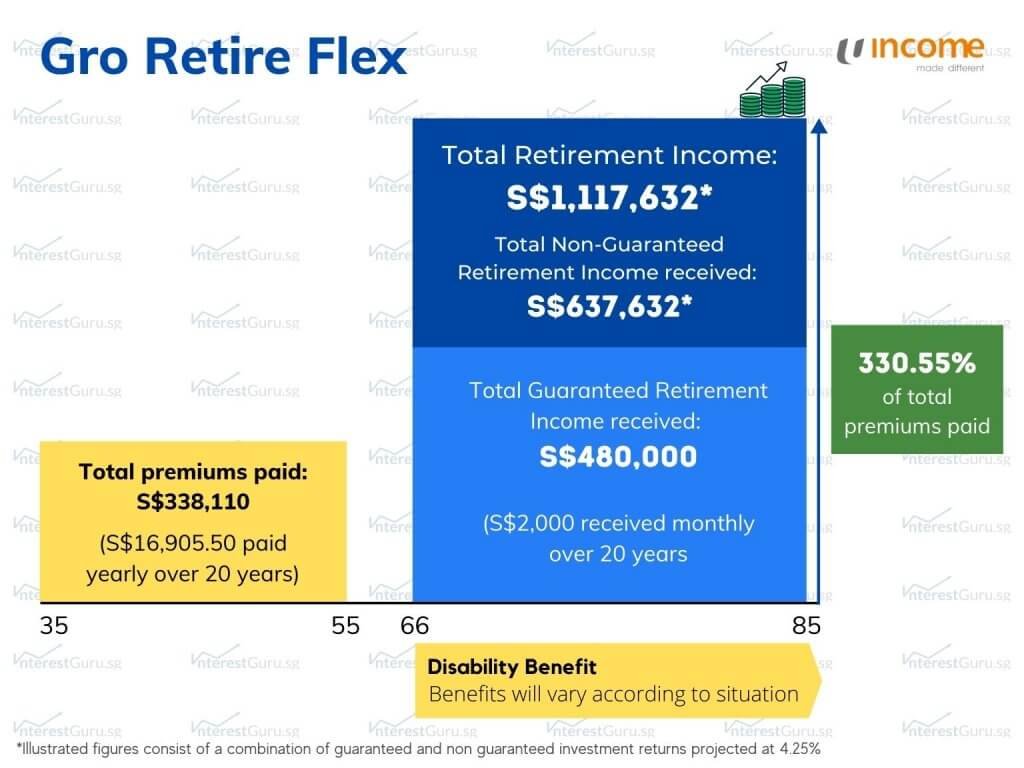

At age 35, Ben purchases NTUC Income Gro Retire Flex to plan for his retirement. He pays a yearly premium of S$16,905.50 for the next 20 years.

With a total of S$338,110 paid in premiums, the policy continues accumulating cash value with no further financial commitment until the chosen retirement age. At age 66, Ben starts receiving a projected retirement monthly income of S$4656.80 for the next 20 years.

By age 85, Ben received a total of S$1,117,632 in projected retirement income with only S$338,110 paid in premiums, a good 330.50% return on his investment.

Conclusion of NTUC Income Gro Retire Flex’s Policy Illustration

Through this illustration, we have found that NTUC Income Gro Retire Flex gives the highest guaranteed income with the lowest premiums.

This is good news for those who seek a retirement plan with a high guaranteed monthly income for the lowest cost.

What we like about NTUC Income Gro Retire Flex

- All future premiums waived with NTUC Income Disability Care Benefit

- 2x of guaranteed monthly income with NTUC Income Disability Care Benefit

- An additional lump sum in the event of disability before your desired retirement payout age

- 100% principal guaranteed upon reaching retirement age

What we do not like about NTUC Income Gro Retire Flex

- Disability Care benefit pays you at max an additional 50% while Singlife Flexi Retirement pays 100% additional (2X the GMI)

More about: NTUC Income Gro Retire Flex (The complete policy review)

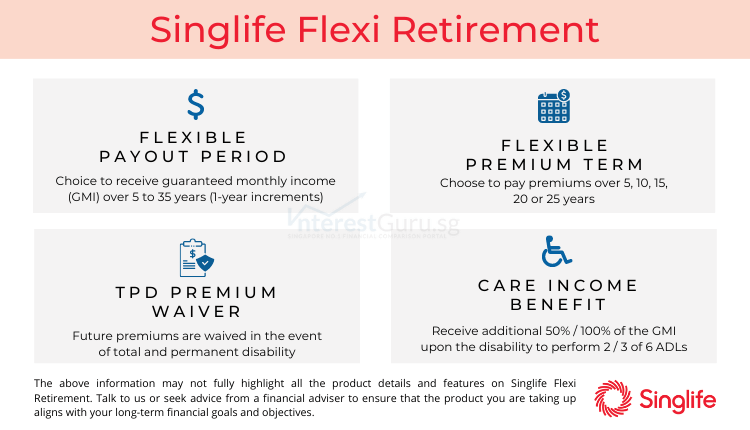

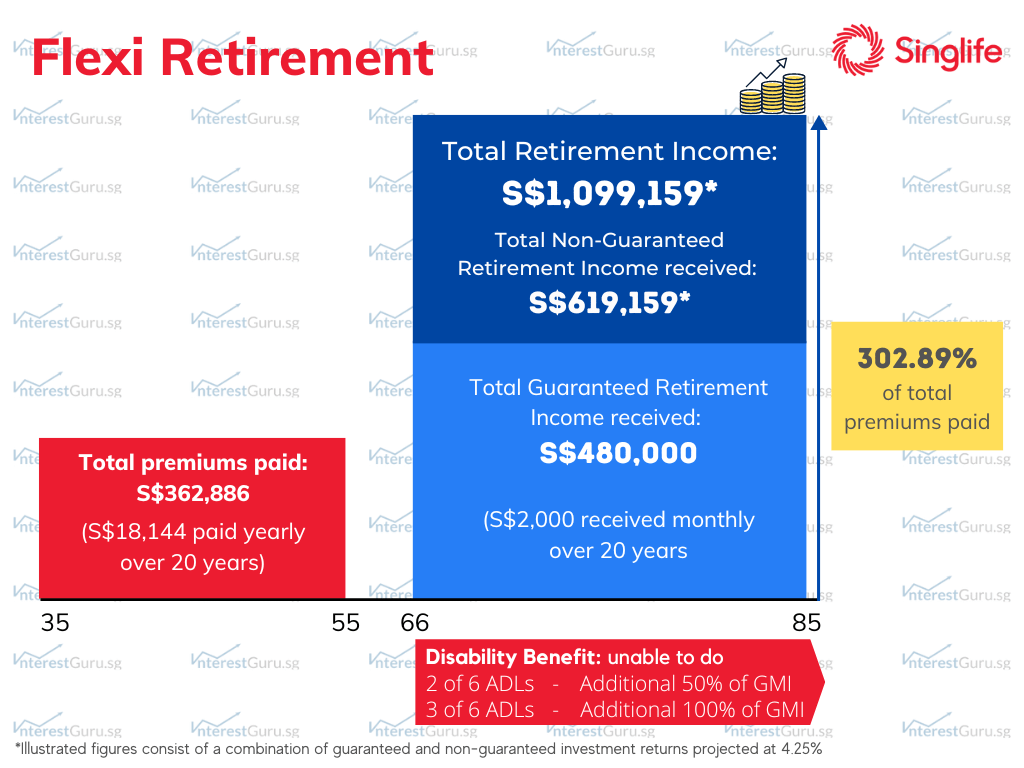

Best High Income Retirement Plan for Disability Benefit – Singlife Retirement income

Singlife Flexi Retirement (previously known as Aviva MyRetirement Choice III) remains one of the most competitive annuities in Singapore. This is a regular premium retirement plan which you can customize based on your desired lifestyle and finances.

Flexi Retirement will be 100% principal guaranteed upon reaching your chosen retirement age and comes with Care Income Benefits which is equivalent to your monthly guaranteed income payable should you not be able to perform 3 out of 6 Activities of Daily Living (ADLs).

Singlife Flexi Retirement gives you the option to choose:

- Your preferred retirement age

- Your preferred amount of monthly guaranteed income

- Your preferred number of years (5 to 35 years) to receive your monthly payout

- Your preferred premium term of 5, 10, 15, 20 or 25 years

- Hassle-free application – No health underwriting needed

In-depth financial details for Singlife Flexi Retirement

At age 35, Carol purchases Singlife Flexi Retirement to plan for her retirement. She pays a yearly premium of S$18,144 for the next 20 years.

At age 66, Carol is eligible to receive a non-guaranteed bonus which she instead chooses to convert to additional monthly income.

With a total of S$362,886 paid in premiums, Carol starts receiving a total projected retirement income of S$4579.80 per month for the next 20 years.

Should Carol lose her ability to perform 2 of the 6 ADLs, she will receive an additional S$1,000 per month of retirement income. If she lost the ability to perform 3 of the 6 ADLs, she will receive a total additional of S$2,000 per month.

Otherwise, by age 85, Carol would have received a total projected S$1,099,159 in retirement income with only S$362,886 paid in premiums, a grand 302.89% return on her investment.

Conclusion on Singlife Flexi Retirement’s Policy Illustration

The most flexible retirement plan in the market allows you the flexibility to retire anytime you want. Although the premiums are a little high amongst the other retirement plans here, its non-guaranteed portion makes up for that, giving you the highest return on investment.

Related article: How can I accumulate a million dollar (Realistically)

What we like about Singlife Flexi Retirement

- Flexibility to choose your retirement age. You do not need to choose between 55, 60, 65. You are free to choose when you want to retire or even retire earlier than 55 years old

- 100% principal guaranteed upon reaching retirement age

- No health underwriting needed

- Option to receive a non-guaranteed bonus in a lump sum or spread it into your monthly income at the start of your chosen retirement age

- 2X of monthly Guaranteed Income – Upon unable to perform 3 out of 6 ADL

- Easy Term rider – Lump sum payment in the event of Death, Terminal Illness or Total permanent disability

**Although there is no single premium option, this is the only 5-year premium term retirement plan/ annuity policy with comparable or even higher returns to a single premium policy (Verified by Benefit Illustration provided by our licensed financial advisers).

What we do not like about Singlife Flexi Retirement

- Lack of Single Premium option choice, minimum premium payment tenure is 5 years

- Cash option only. You are not allowed to use your funds from your CPF SRS account

- Unlike Manulife RetireReady Plus II, there is no coverage for the disability to perform 2 ADLs

More about: Singlife Flexi Retirement (The complete policy review)

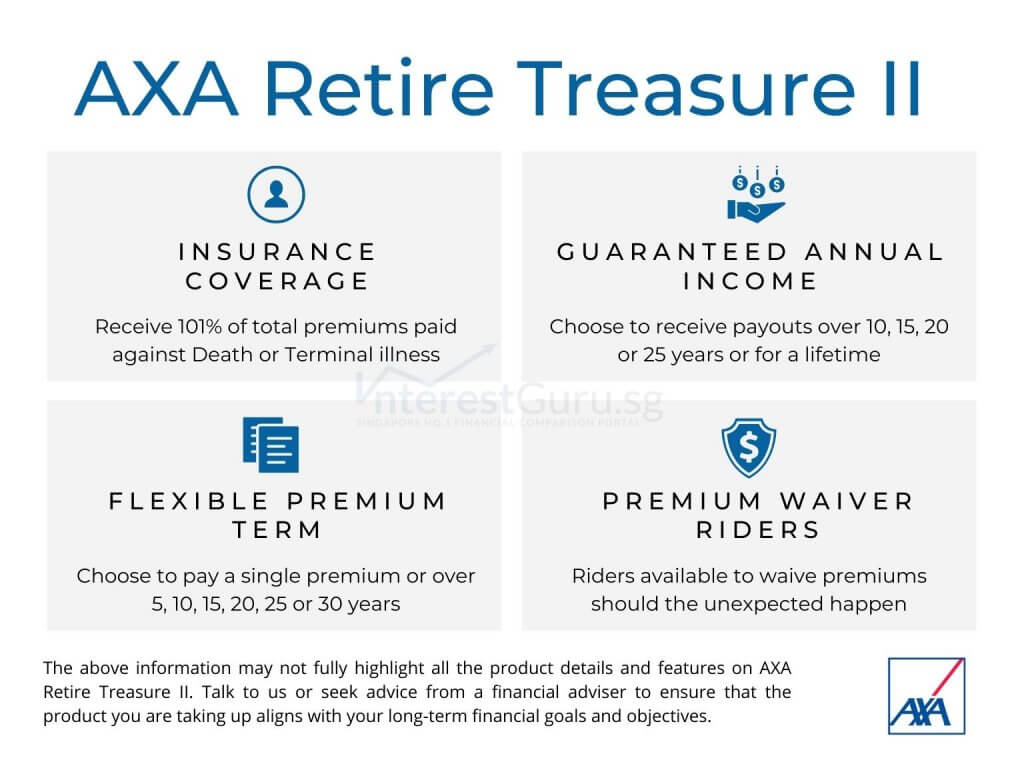

Best High Income Retirement Plan For Lump-sum Payout – AXA Retire Treasure II

The latest addition to the best retirement plan for high income, AXA Retire Treasure II gives you the non-guaranteed retirement income in form of a maturity benefit. If you are looking to receive a lump-sum amount upon reaching the end of your retirement plan, AXA Retire Treasure II may be the retirement plan for you.

AXA Retire Treasure II gives you the flexibility to choose:

- Your preferred premium payment term (Single premium, or 5 to 30 years, 5-year intervals)

- Your prefered payout term (Lifetime; till age 120, or 10 to 25 years, 5-year intervals)

- Your preferred guaranteed monthly income

- The option to add a secondary life assured (to continue receiving the benefits of the policy upon your death)

- SRS fundable

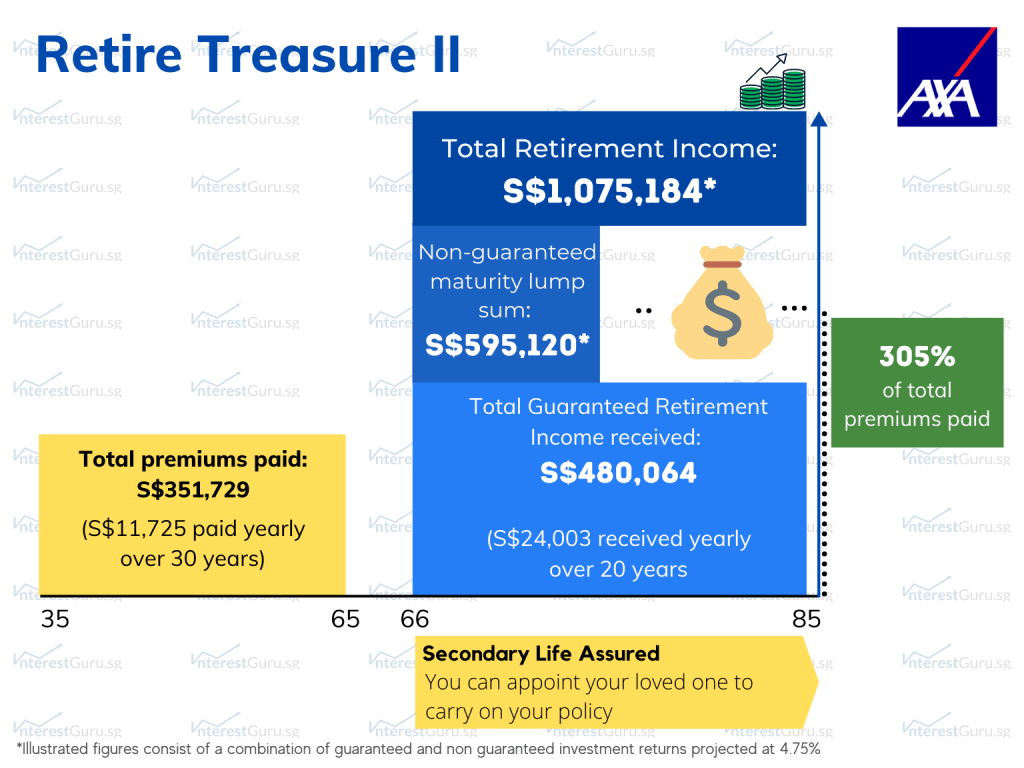

In-dept policy illustration for AXA Retire Treasure II

At age 35, John purchases AXA Retire Treasure II to plan for his retirement. He pays a yearly premium of S$11,725 for the next 30 years.

With a total of S$351,729 paid in premiums, John starts receiving guaranteed retirement income of S$24,003 per year for the next 20 years.

Upon reaching age 85, John’s AXA Retire Treasure II plan comes to an end, giving him a non-guaranteed maturity lump-sum bonus of S$595,120.

John received a total of S$1,075,184 in retirement income with only S$351,729 paid, a good 305% returns on his investment.

Conclusions on AXA Retire Treasure II’s Policy Illustration

At the end of the policy, AXA Retire Treasure II gives you a lump-sum bonus which you can use according to your wish and goals.

What we like about AXA Retire Treasure II

- AXA Retire Treasure II allows you to add a secondary life assured, this means your loved one can carry on receiving retirement income after your passing. This is especially beneficial if you choose to receive lifetime payout as the policy matures on the 120th anniversary of your life

- This retirement plan is fundable using your CPF SRS funds

What we do not like about AXA Retire Treasure II

- AXA Retire Treasure II pays out retirement income yearly. This is a downside for those who prefer to receive their retirement income on a monthly basis

Detailed comparison for retirement plans based on features and income payout

We have compiled a detailed data based on age 35 with the intention to pay insurance premiums for 20 to 30 years. The aim here is to receive the highest initial and guaranteed income payout starting at age 66, lasting for 20 years to age 85.

At the same time, an emphasis is made on features that double the guaranteed monthly income in the event of severe disability. The rationale is not to have your income payout diluted by the cost for long-term and medical expenses during your retirement.

Note: For users on mobile devices, you may have to swipe/ scroll on the chart to view the complete data.

| High-income payout retirement plans for: Male, Age 45, Retire at Age 65 |

||||

| Plan Details |  Manulife RetireReady Plus II (Payout for 20 years) |  Aviva MyRetirement Choice II (Payout for 20 years) |  NTUC Income Gro Retire Ease (Payout for 20 years) |  AXA Retire Treasure II (Payout for 20 years) |

| Annual Premium | $13,536 Pay premium for 20 years Total Premium paid: $270,720 | $18,539.75 Pay premium for 20 years Total premium paid: $370,795 | $9,828.05 Pay premium for 26 years Total premium paid: $255,529 | $11,725 Pay premium for 30 years Total premium paid: $351,729 |

| Yearly Income Payout (Guaranteed/ Projected) | $24,000/ $47,942.28 | $24,000/ $72,375.96 | $24,000/ $42,825.60 | $24,003 (Guaranteed) |

| Total Guaranteed Payout (Guaranteed only) | $480,000 | $480,000 | $480,000 | $480,064 |

| Total Projected Payout (Guaranteed and Non-Guaranteed) | $958,845 | $1,447,520 | $856,512 | $1,075,184 (Including projected maturity bonus of S$595,120) |

Additional note:

|

||||

How do you get the most out of your retirement plan?

Your retirement plans are meant to supplement your lifestyle and expenses in your golden years. Find a retirement plan that pays out according to your life objectives before looking at the financial figures.

After all, the yields and the financial payout will not make a difference if the retirement plan does not allow you to utilize it according to your retirement lifestyle.

Related article: 5 reasons to invest in a retirement annuity plan *NEW*

Whenever possible, consider the following before taking up a retirement plan:

- Would you prefer a higher guaranteed or a higher overall non-guaranteed payout?

- Do you need the payout to increase at a fixed rate to keep up with inflation?

- In the event of disability or Critical Illness, do you still have to continue paying your premiums?

- What is the overall annualised yield on the retirement plan?

- Are you expecting a lump sum payout once you reach your retirement age?

- How much guaranteed and non-guaranteed are you expected to receive if you have to do an early surrender of your policy during your retirement years?

- In the event of disability during the payout period, is there any income multiplier to cover additional costs that will be incurred on your lifestyle?

Ensure that your retirement plan can address your retirement needs and concerns as much as possible. Due to the large financial commitment and long time horizon required, never compromise on what is important to you.

Drop us a message to have a retirement plan structured to your needs or just to understand more.

What are the other alternatives besides a high income retirement plan?

A retirement plan with the highest income payout allows greater financial freedom during your initial retirement years. You may also wish to explore having a separate retirement plan to provide additional financial security with some of the unique features below:

- Additional guaranteed monthly payout, in the event of failing minimally 2 out of 6 or 3 out of 6 activities of daily living.

- A retirement plan that only payouts monthly over the next 10/15 years from the start of your retirement, but provide a lump sum cash payout at maturity.

- Lower monthly payout, but the plan guarantees a lifetime payout, with the option to pass on the plan to the next generation.

- Lower initial monthly payout but payout increases yearly to keep pace with inflation.

- Making withdrawal only as need via a lifetime whole life savings plan, while allowing un-utilised savings to generate returns in the plan.

- Investing into a basket of unit trust funds that provides a higher non-guaranteed monthly payout.

While the income payout from the above list of plans may not be as high as a high income payout retirement plan, each of the said categories may offer unique financial benefits to you.

What are the best retirement annuity plans for you?

Wish to know more about how the above retirement plan or annuity policies fit into your financial and insurance portfolio?

Use our retirement planning selector to get INSTANT QUOTES based on your individual profile now!

Find the best retirement plans and annuity policies with the highest income payout here!

Our partnered financial planners will draft their proposals based on your given input. Your information and details will only be used for communication with you.

All comparisons done are solely based on your individual needs.

Frequently Asked Questions (FAQs)

Question: What are the premium terms for whole life insurance plans?

- Answer: Whole life insurance premium terms usually go for 5, 10, 15, 20, 25, 30 years or up till age 65.

Question: How long does whole life insurance plans cover me for?

- Answer: Whole life insurance plans generally cover you till age 99 or when the benefits are fully paid out.

*For a limited time, get attractive incentives when you take up any product that is proposed by our team of financial planners.

Compare retirement annuities plans quotations from all leading insurers in Singapore!

Getting the best retirement plans has never been this easy!

Drop us a message to have a retirement plan structured to your needs by a licensed financial adviser. Don’t worry, there is no obligation to take up anything and consultation is 100% free!

Best Insurance Plans in Singapore

Note: All financial figures are based on close approximate and all non-guaranteed figures are based on the higher tier of 4.75% investment returns. The sample illustrations are for illustrative purposes only and is not a contract of insurance. Early surrendering or cashing out from Retirement plans or Annuity policies will certainly result in financial loss. In the event of doubt, always refer to the precise terms and conditions as specified in your policy contract. Seek the advice of a qualified financial professional or a licensed financial adviser before making any decision or financial commitment.

*Terms and conditions may apply, speak to our financial planners or drop us a message for more details.

Latest Change Log for 3 Best Retirement Plans in Singapore (Features and Income payout)

Version 1.7 – 16/04/2023

- Updated alternatives plans and retirement options besides getting a high payout income retirement plan

Version 1.6 – 18/03/2023

- Additional best retirement plan – AXA Retire Treasure II

- Revamped examples of each best retirement plan

Version 1.5 – 14/10/2023

- Alternatives to high income retirement plans

Version 1.4 – 3/8/2023

- Minor text edits

- Updated links to related retirement planning contents

Version 1.3 – 8/7/2023

Manulife RetireReady is replaced by Manulife RetireReady Plus II due to

- Manulife RetireReady is no longer available

- Manulife RetirerReady Plus guaranteed income multiplier now partially kicks in upon failing 2 of 6 ADLs.

Version 1.2 – 24/6/2023

AXA Retire Happy Plus is replaced by NTUC Income Gro Retire Ease due to:

- A lower annual premium for NTUC Income Gro Retire Ease for the same guaranteed income

- Additional 2x guaranteed Income for severe disability built into NTUC Income Gro Retire Ease

- More competitive overall returns

Version 1.1 – 3/4/2023

Aviva MyRetirement Plus is replaced by Aviva MyRetirement Choice II due to:

- A lower annual premium for Aviva MyRetirement Choice II

- Higher initial income payout for Aviva MyRetirement Choice II

- Additional 2x guaranteed Income for severe disability built into NTUC Income Gro Retire Ease

- However, Aviva MyRetirement Plus STILL OFFERS a higher overall payout at the cost of a lower initial payout