Take a favourite item from your childhood or teenage years, how much has its price went up as of now?

The current financial outlook

After a prolonged period of low inflation due to global fiscal stimulus, inflation is on board again. Major economic powerhouses, the US and China are both tightening fiscal policies. The US Feds is planning another two rounds of interest rate hikes for 2023. China is raising the interest rates it charges in open-market operations and short-term lending (repo) rates.

The financial impact on the increase in interest rate will certainly be felt both globally and locally in Singapore.

What does this mean for my savings?

As of May 2023, the Consumer Prices Index (CPI) in Singapore rose by 1.4% on a year-on-year basis. All Items Less Accommodation stands at 2.2% in May 2023 on a year-on-year basis.

The increase is driven higher due to: Prices of food at 1.5%, clothing and footwear at 1.9%, healthcare at 2.4% and transport at 3.8%.

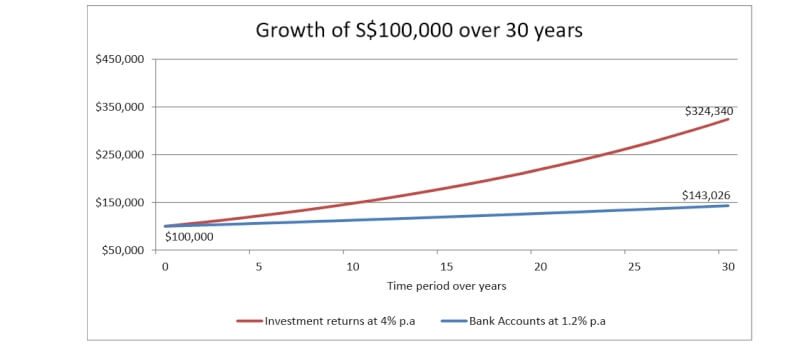

Basically, if your savings is generating less than 1.5% return per annual, you will worse off financially compared to last year. This is due to a decrease in your purchasing power.

Source: SPrice Index, SingStat.gov.sg (Open in new window)

What can I do to about rising inflation?

We round out the 5 best ways you can get more out of your money:

Minimise cash saving

You will still need to have emergency funds set aside, but cash is no longer king. At least, not in a rising interest rate environment. The interest rate will always be lower than the inflation rate, meaning wealth is actually transferred from savers to borrowers.

Generating real financial return does not equate to high financial risk. Minimised your risk by diversifying your investment assets.

Read about: Investing Basics: Risk profile and Investment Portfolio

Read about: Investing Basics: Diversification

Invest in equities

Investing in equities over a long-term horizon provides one of the best options available to beat inflation. In a rising inflation environment, companies will certainly pass on the increase in costs incurred for its product to the consumer. On the other hand, the consumers can only choose between the most competitive options available for the said product. Being an investor and owning a share of a company allows an individual the opportunity to take part in the overall economic growth.

With reference to the S&P 500 chart below: Even if you had invested during the peaks of 2000 or 2007-2008, you would still be making a decent financial gain had u held on to your investment. Clearly, if you had invested during any other time period, your financial gains would be even higher. Either way, beating inflation is not an issue here.

Source: S&P 500 chart, nasdaq.com (Open in new window)

Those wishing to diversify their investment may also consider suitable Unit Trust Funds or ETFs. Your money is pooled or combined with money from other investors and invested according to the fund’s investment objective. This allows wider access to funds/ investment in financial instruments such as equities, bonds, commodities or other asset classes that you otherwise might not have access to in your own Investment Portfolio.

Read about: ETF or Unit Trust: Which is suitable for me?

Read about: Managing your Investment Portfolio

Hedge your equities risk with bonds

Government and investment graded bonds may offer a moderately higher financial yield than the current interest rate. However, the stability and security offered means that it is sensitive to interest rates change. If interest rates subsequently increase to a higher level than the yield offered by the bond you are holding on, expect the face value of the bond to be reduced. Similarly, if interest rates fall, expect the face value to appreciate.

During a period of financial uncertainty, the interest rate will go down due to an easing of monetary policy to stimulate economic growth. Institutional and retail investors will flock to bonds, making it a good hedge against equities while offering a higher yield than bank accounts.

Investment grade bonds are usually in coupons of 250,000 SGD, making it highly inaccessible to the retail investors. Consider Trust Funds that invest in a basket of bonds securities. Those seeking a regular income stream from their investment may also look into Income Funds which seeks to provide a consistent payout.

Related: Bonds

Read about: Income Fund, Investing Guide: Reasons to invest in Unit Trusts

Own physical assets

When inflation greatly exceeds interest rate growth, cash loses real purchasing power quickly. This is when “physical assets” such as property, commodities such as gold and silver held its value. An increase in price enhance property resale prices and also command higher rental yield. Gold also acts a hedge against currency depreciation, with its value at its highest when governments and central banks are easing monetary policies.

Another option includes investing in companies that are involved in the building of infrastructure. This provides a hedge against inflation as there is usually an increase in construction during a period of easing monetary policies and low-interest rate environment. The reason behind this being that the building and construction industry require labours and manpower, which in turn support jobs creation and income.

This is also known as the recovery phase in the market cycle and you should look for funds that invest mainly in Infrastructure, Industrial and Raw Material.

Read about: Investing Basics: Market Cycles

Look into alternative saving method

If you are heavily invested in the above or the risk involved is simply unbearable, consider other saving options. Step-up interest saving account may allow a higher interest. This is provided that specific conditions such as credit card, Giro payment, investment and insurance products are taken up with the bank.

Endowment policy consists of saving elements that pay out a lump sum after a specific tenure. The flexibility of partial withdrawal provided allows liquidity in times of extreme needs. Similarly, other Life Insurance product may provide guaranteed principle and financial returns upon maturity of the said product. This allows future financial goals or objectives to be met with higher financial certainty, at the cost of lower returns compared to investing.

Your Insurance Portfolio can do more than providing Health and Insurance coverage. You should speak to an experienced wealth planner which should guide you through your financial planning process.

Related: Endowment and Saving Policy

Read about: Managing your Insurance Portfolio

Read about: How are the financial goals you set for 2023 working out?

There is no guarantee that the above guide will certainly beat inflation, and investment risk should be spread out by diversifying into different asset classes. Start by having sound financial management and prudent planning. Seeking a higher financial return to beat inflation is not rocket science!

Drop us a message if you are looking for more information on any of the above.