An early critical illness plan provides coverage against ALL stages (early, immediate and advance) of a critical illness. Find out about the best early critical illness plans across all insurers in Singapore!

Related: Which critical illness insurance plan is the best for critical illness coverage *NEW*

What are the Best Early Critical Illness Plans in Singapore?

InterestGuru.sg reviewed early critical illness plans from all insurers in Singapore for product features and benefits.

- Best Early Critical Illness Plan for Cheapest Premium: Aviva MyEarly Critical Illness Plan II

- Best Early Critical Illness Plan for Comprehensive Coverage: Manulife ReadyComplete Care

- Best Early Critical Illness Plan for Multiple Insurance Claims: Aviva MyMultiPay Critical Illness Plan IV

- Best Early Critical Illness Plan for Premium Wavier: Tokio Marine TM EarlyCover

- Best Early Critical Illness Plan for Seniors (age 50 and above): NTUC Income Silver Protect

How did we come out with this list of the 5 Best Early Critical Illness Plans in Singapore?

The criteria being used to select the best early critical illness plans are based on their unique product features and benefits are as below:

- Usefulness of unique product features

- In-depth policy conditions for making an early critical illness claim

- Number of covered medical conditions

- Overall insurance premium payable compared to competitor plans

- Additional insurance premium payable against provided benefits

Note: The early critical illness plans listed below are not ranked in any priorities or preferences. Speak to a licensed financial adviser to ensure your early critical illness insurance plan is customized accordingly to your needs.

Best Early Critical Illness Plan for Cheapest Premium: Aviva MyEarly Critical Illness Plan

Aviva MyEarly Critical Illness Plan is a simple “no-frill” early critical illness plan with the cheapest premium in Singapore. This early critical illness plan pays out 100% of the sum assured upon the diagnosis of any stage of critical illnesses with coverage up to age 99.

Additionally, Aviva MyEarly Critical Illness Plan covers you for 18 special benefits for 25% of your sum assured (Cap at $25,000 each) without compromising the critical illness coverage amount. The special benefits feature covers medical conditions such as diabetic complications and osteoporosis and can be claimed up to a maximum of 6 times.

Sample case study for Aviva MyEarly Critical Illness Plan

Mary (female, age 30, non-smoker) wish to get coverage for any stages of a critical illness until her retirement at age 65.

- Early Critical Illness sum assured at: $100,000 (Covers all stages of critical illness)

- Policy Term: 35 years

- Premium Term: 35 years

Sample financial illustration for Aviva MyEarly Critical Illness Plan

Based on the above case study, Mary insurance premium will be:

- $818 per year

Upon a claim payout for critical illness, the policy and coverage will terminate and no future premium will be payable.

Refer to: Aviva MyEarly Critical Illness Plan I review

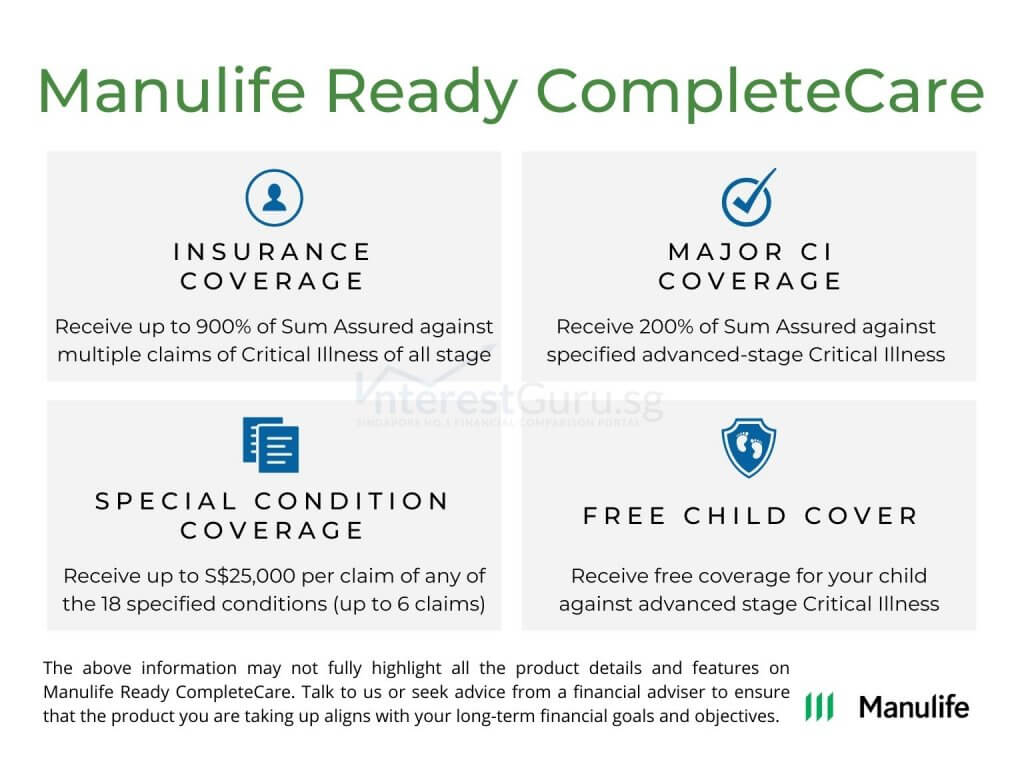

Best Early Critical Illness Plan for Comprehensive Coverage: Manulife ReadyComplete Care

Manulife ReadyComplete Care is a comprehensive critical illness plan that covers all stages of critical illnesses. With its “cover me again” rider, you get coverage up to 500% of your chosen sum assured. ReadyComplete Care also comes with additional benefits for your health and your family.

Get additional benefits including:

- Free medical checkup every 2 years

- Free child coverage against advanced stages of critical illnesses

- Premium refunded in the event of your death

Sample case study for Manulife ReadyComplete Care

Joe (male, age 30, non-smoker), would like to purchase Manulife Ready CompleteCare with Cover me again benefit. He wishes to be covered for $150,000 until age 75, with “cover me again” benefits.

- Policy sum assured at: $150,000 (Covers all stages of critical illness)

- Policy Term: 45 years

- Premium Term: 45 years

Sample financial illustration for Manulife ReadyComplete Care

Based on the above case study, Joe insurance premium will be:

- $2,127 per year (Including “Cover me again” rider)

If Joe did a claim on critical illness once, a $150,000 sum assured will be paid to him. With cover me again benefit, his sum assured will be restored back to $150,000 again after 12 months, until 500% of sum assured is claimed.

Refer to: Manulife Ready CompleteCare review

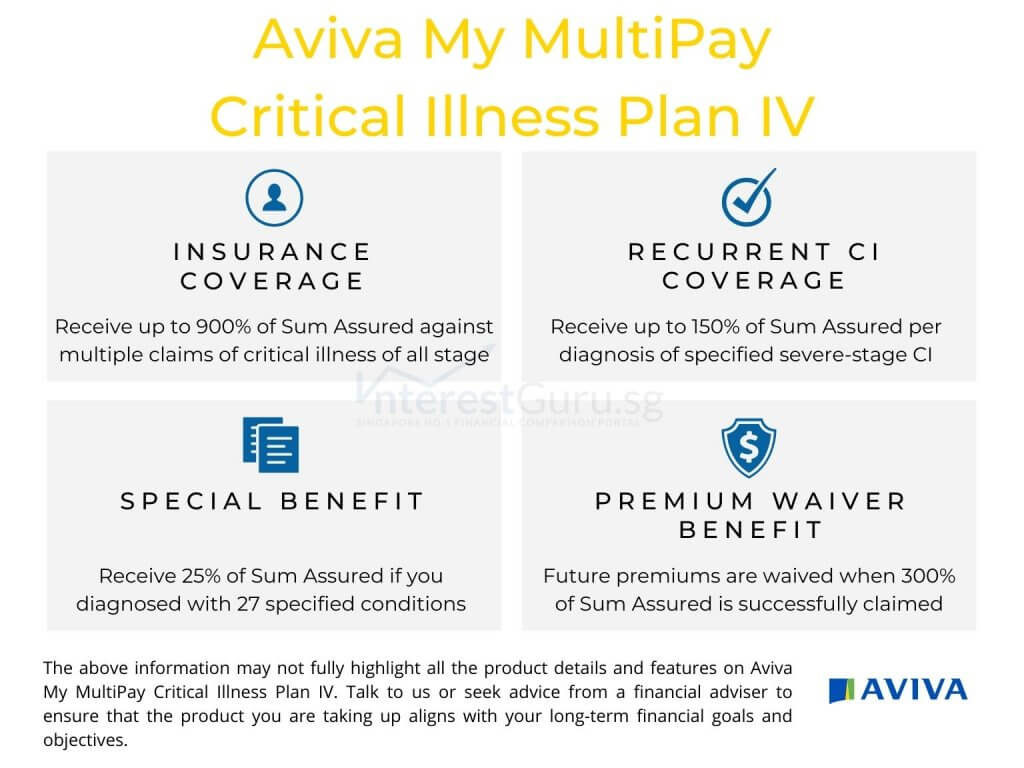

Best Early Critical Illness Plan for Multiple Insurance Claims: Aviva MyMultiPay Critical Illness Plan III

Aviva MyMultiPay Critical Illness Plan III is a competitive early critical illness plan with claims payable for all stages of critical illnesses. This early critical illness plan from Aviva also has the highest multiple payout features at 600% of your sum assured.

With Aviva MyMultiPay Critical Illness Plan III, you can claim for lump sum payout of

- Early or Intermediate Stage of Critical Illness (2 times each of 100% sum assured )

- Critical Illness (1 time at 300% of sum assured, less payout for Early or Intermediate Stage)

- Major cancers, Heart attack or Stroke (150% of sum assured)

- Recurrent Major cancers, Heart attack, Stroke (150% of sum assured)

Aviva MyMultiPay Critical Illness Plan III also covers you for 24 special benefits for 25% of your sum assured (Cap at $25,000 each) without compromising the critical illness coverage amount. The special benefits feature covers medical conditions such as diabetic complications and osteoporosis and can be claimed up to a maximum of 6 times.

Sample case study for Aviva MyMultiPay Critical Illness Plan III

Chloe (female, age 30, non-smoker), would like to purchase Aviva MyMultiPay Critical Illness Plan III for the multiple early critical illness claim features. She wishes to be covered for $150,000 until age 70.

- Policy sum assured at: $150,000 (Covers all stages of critical illness)

- Policy Term: 40 years

- Premium Term: 40 years

Sample financial illustration for Aviva MyMultiPay Critical Illness Plan III

Based on the above case study, Chloe insurance premium will be:

- $1,798 per year

Chloe will be covered for early, intermediate and advanced stages of critical illness to age 70 or until the policy has paid out $900,000 (600% of sum assured).

Refer to: Aviva MyMultiPay Critical Illness Plan IV review

Best Early Critical Illness Plan for Premium Wavier: Tokio Marine TM EarlyCover

Upon the first successful claim of an early or intermediate stage critical illness (Cap at $350,000 for early critical illness), all future premiums for your Tokio Marine TM EarlyCover plan will be waived. To take advantage of the premium waiver feature, a high sum assured of above $350,000 would allow your policy to stay in force after your first payout.

Sample case study for Tokio Marine TM EarlyCover

Melvin (male, age 30, non-smoker), seek to have high early critical illness coverage while having continual coverage and future insurance premium waived. He chooses to take up a TM EarlyCover with a sum assured of $500,000 to age 70.

- Policy sum assured at: $500,000 (Cap at $350,00 for early critical illness payout)

- Policy Term: 40 years

- Premium Term: 40 years

Sample financial illustration for Tokio Marine TM EarlyCover

Based on the above case study, Melvin insurance premium will be:

- $3,005 per year

In the event of a successful early critical illness claim, Melvin will receive a lump sum payout of $350,000. All future premium for the policy will be waived and the remaining sum assured of $150,000 will be claimable in the event of an intermediate/ advanced stage of a critical illness.

Refer to: Tokio Marine TM EarlyCover review

Best Early Critical Illness Plan for Seniors (age 50 and above): NTUC Income Silver Protect

NTUC Income Silver Protect is an early critical illness plan specially made for those age 50 and above. Not only is a medical check-up not required to sign up for the policy, but renewal is also guaranteed every 10 years.

The entry age for NTUC Income Silver Protect is from 50 to 74 years old (last birthday), for a coverage term of 10 years. This early critical illness plan with provide coverage up to a maximum age of 84 (last birthday).

Have a pre-existing or existing medical condition?

You may still be able to take up NTUC Income Silver Protect if the pre-existing medical condition is non-cancer related.

Sample case study for NTUC Income Silver Protect

Mdm Lee (female, age 50, non-smoker), is aware that getting early critical coverage will be very expensive via a typical critical illness insurance plan. Instead, she chooses to take up an NTUC Income Silver Protect with the maximum assured amount of $100,000.

- Policy sum assured at: $100,000

- The payout for early critical illness is cap at 25% of sum assured

- The payout for critical illness at 100% or 125% of sum assured

- Accidental fractures coverage: Up to 20% of sum assured

- Policy Term: 10 years

- Premium Term: 10 years

Sample financial illustration for NTUC Income Silver Protect

Based on the above case study, Mdm Lee insurance premium will be:

- $940 per year

The renewal of the NTUC Income Silver Protect is guaranteed when her plan expires at the end of the 10th year.

Refer to: NTUC Income Silver Protect review

What other options should you consider besides an early critical illness plan?

If the only shortfall in your insurance coverage is for early critical illnesses, an early critical illness plan or a term life insurance plan will provide the best value for your money.

However, if there is an overall shortfall in your insurance coverage, alternative options may provide better a value for your money.

You may wish to consider the following life insurance policies that provide high early critical illness coverage, along with other useful features and benefits.

- Term Life Insurance Plans – Provides high coverage for all your insurance needs

- Whole Life Insurance Plans – Provides lifetime insurance coverage with stable wealth accumulation

Read about: 3 things to consider before taking up a new financial product

Read about: How much life insurance coverage do you need in Singapore?

An alternative to early critical illness plans: Whole life insurance plans

In your 20s or early 30s, the total premium paid over a limited period for a whole life plan may end up being lower compared to an early critical illness plan. Not only is the overall premium lower, but a whole life plan will also accumulate a guaranteed cash value that increases over time.

The accumulated cash value can be withdrawn at your later life stages for other financial goals, such as a lump sum retirement payout or a monthly income stream.

Read about: 3 Best Whole Life Plans for Coverage and Wealth Accumulation (2023 Edition)

Read about: 8 Best Whole Life Plans in Singapore based on Product Features (2023 Edition)

An alternative to early critical illness plans: Term life insurance plans

A term life insurance plan can also provide a high level of coverage for all your insurance coverage needs, for an affordable yearly premium. Your coverage amount can be customised based on your need, including but not limited to the following:

- Death

- Total and Permanent Disability

- Critical Illness

- Early Critical Illness

Similar to an early critical illness plan, a term life plan also does not accumulate cash value over time. This means that the premium paid for the period of coverage is not recoverable if no claims were made from the term life plan.

Read about: 8 Best Term Life Insurance Plans in Singapore based on Product Features (2023 Edition)

Read about: Which critical illness insurance plan is the best for critical illness coverage *NEW*

Learn more: Understanding the figures from the insurance coverage calculator

Learn more: How much insurance coverage do you need? (Singapore Edition)

Which early critical illness plans are the most suitable for you?